Updated on February 19, 2026

How Does Loan Application Abandonment Hurt SME Lenders?

The story usually starts well.

A manufacturing SME CFO finally finds a lender that looks promising, clicks “Apply now”, and begins a working capital loan application. Ten minutes in, she hits a wall: the form wants GST returns she doesn’t have on hand, the upload fails twice, and the “Save & continue later” link is buried below the fold. She closes the tab, promising herself she’ll come back later. She never does.

Recent research shows that around two-thirds of consumers now abandon digital financial applications before completion. Signicat’s “Battle to Onboard” study found that 68% of people abandoned a financial services application in the previous year, up from 63% just two years earlier, with billions in acquisition spend effectively wasted on journeys that never convert.

Loan products are hit particularly hard. Industry analyses now describe loan application abandonment rates in the 26–50% range as “common,” with some institutions losing up to 75% of potential loan customers mid-journey.

For SME lenders, the stakes are even higher. Compared to a simple personal loan, SME credit journeys are longer, documentation-heavy, and more complex, which means more opportunities for drop-off. At today’s interest rate levels, each abandoned SME loan application represents not just a lost fee, but years of foregone interest income on larger ticket sizes.

There is market demand for SME loans, but, your loan application pipeline is leaky. This article will unpack why loan application abandonment has become a structural problem in digital lending, we’ll cover:

- Why Is Loan Application Abandonment So Common in Digital Lending?

- How Can Real-Time Intervention Reduce SME Loan Application Abandonment?

- How Can Observability, Data, and AI Help You Detect Drop-Off Risk?

- How Do You Coordinate Human and Digital Support for Complex SME Loan Cases?

- How Can SME Lenders Implement Real-Time Interventions in 60–90 Days?

- How Should You Measure the Impact of Your Loan Application Abandonment Strategy?

- How Do Risk, Compliance, and Customer Consent Shape Real-Time Interventions?

- Conclusion

Why Is Loan Application Abandonment So Common in Digital Lending?

If you zoom out from SME loans for a moment, digital lending has a systemic abandonment problem.

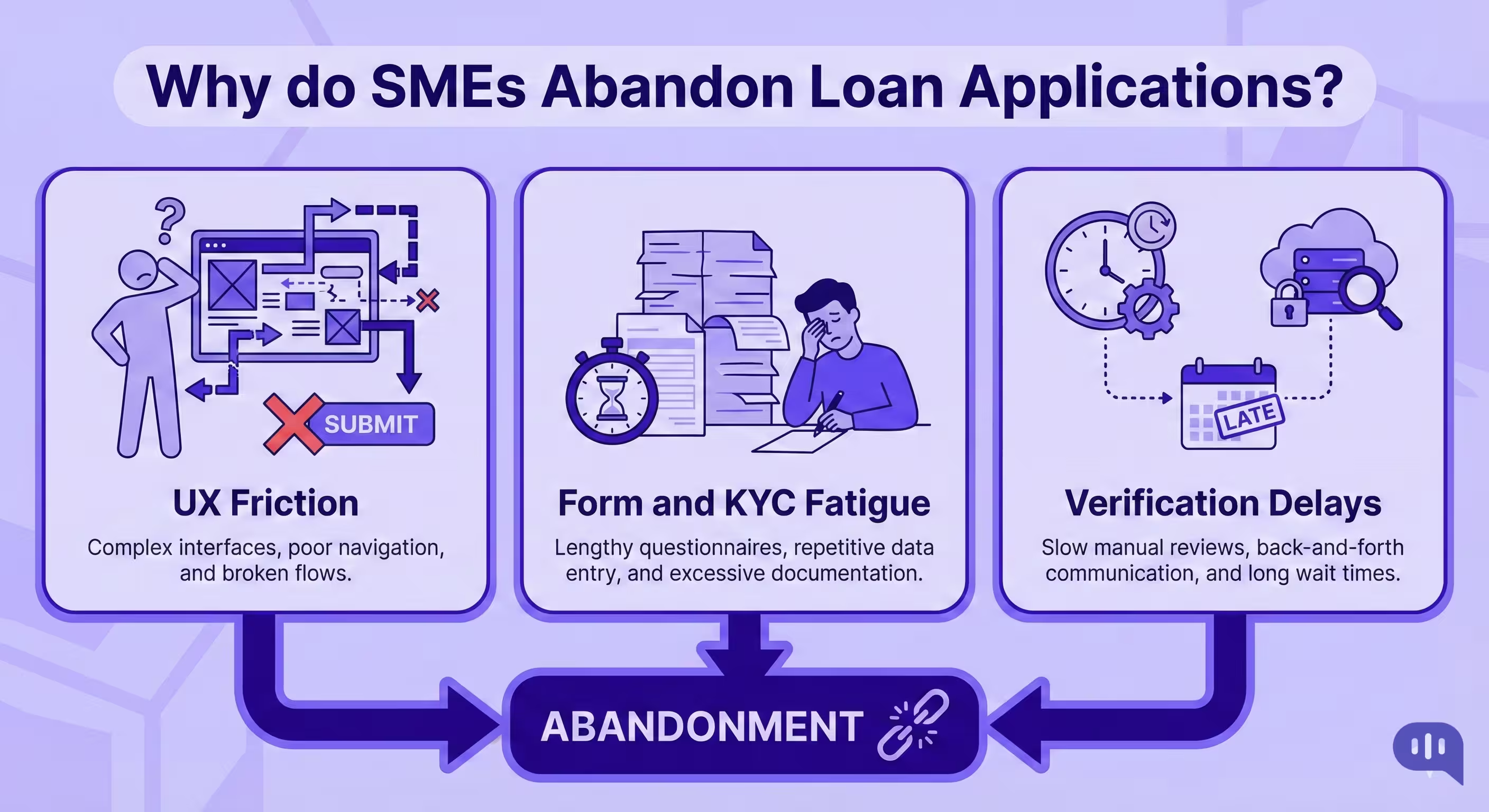

Multiple studies show that well over half of digital banking and lending applications are abandoned before completion. When you look at the underlying reasons, three themes keep coming up:

- Friction everywhere: KPMG’s work on friction in financial services shows that every extra click, form field, or wait time increases the likelihood of abandonment.

- Form and KYC fatigue: Generic web-form research finds that users abandon forms mainly due to length and security concerns. In lending, these issues are magnified by intensive KYC; some studies suggest complex identity verification steps alone can drive up to a 30% increase in abandonment.

- Verification and processing delays: Providers focused on verification (like ComplyCube and others) highlight that long IDVs and slow back-office reviews directly raise drop-off rates, as customers simply give up waiting.

Digital lending journeys ask for a lot, explain very little, and reward patience slowly. That’s a bad recipe in any retail context. For SMEs, it’s even worse.

Why Do SME Borrowers Abandon Digital Loan Applications More Often?

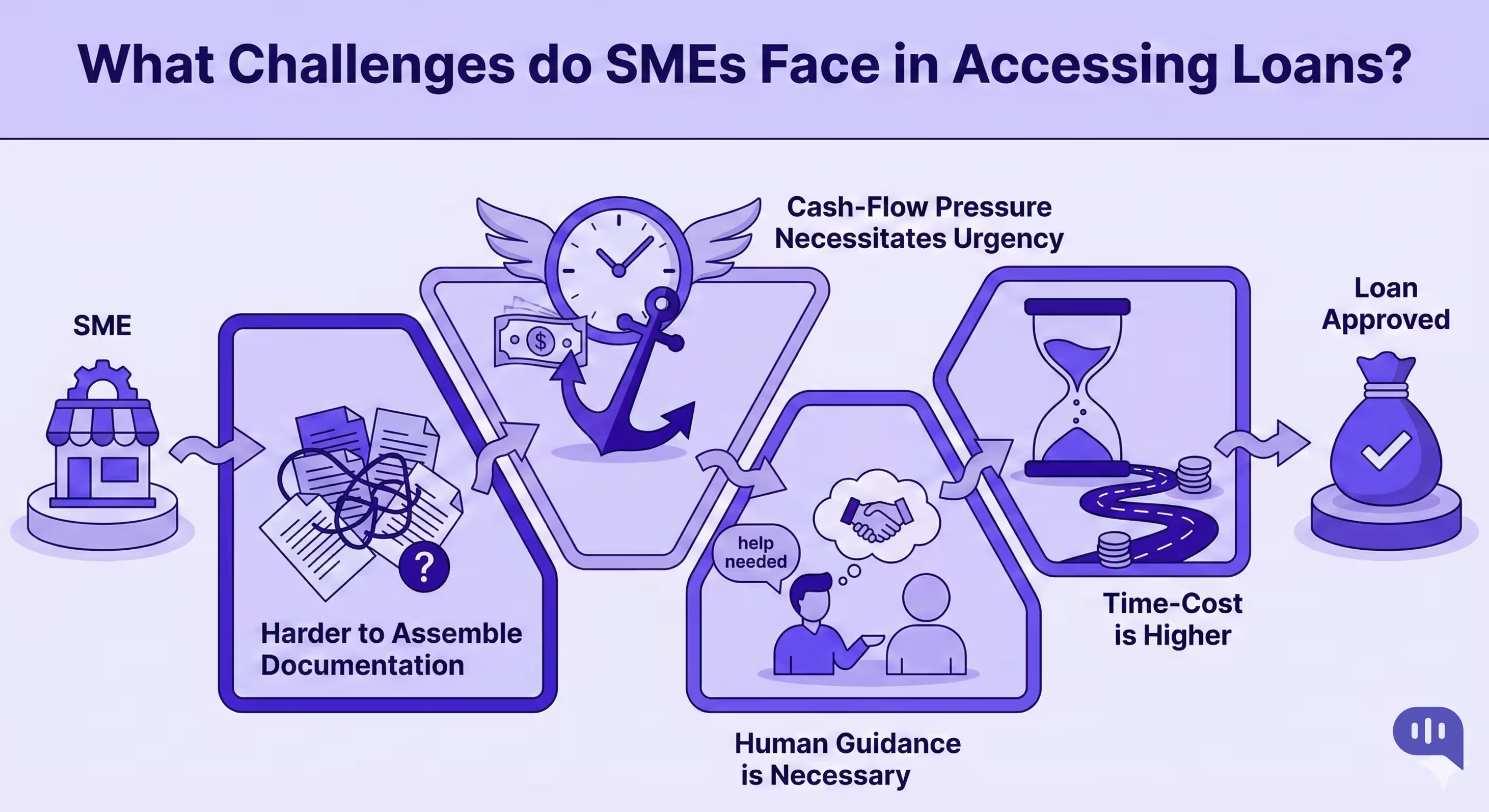

SMEs live in a different reality than retail borrowers, and it shows up in their abandonment patterns.

1. Documentation is Harder to Assemble

SME loans typically require:

- Financial statements and management accounts

- GST / VAT or tax filings

- Bank statements from multiple accounts

- Proofs of ownership, collateral, and sometimes invoices or contracts

Research on MSME finance in emerging markets repeatedly flags documentation and information requirements as a core barrier to accessing credit. Guidance for MSME lenders from IFC notes that traditional processes often expect small businesses to compile data from many systems that were never designed to talk to each other.

So when a digital form suddenly requests six different uploads and doesn’t clearly allow “save and resume,” abandonment becomes the rational choice.

2. Cash-Flow Pressure Makes Time & Uncertainty Harder to Tolerate

Small businesses frequently need funding for near-term cash-flow gaps: payroll, inventory, a large order, or an equipment purchase. This means that extended processing times and legacy workflows put traditional lenders at a disadvantage versus fintechs offering same-day approvals.

If an SME founder feels that:

- the digital application will take days to even get “in review,” and

- there’s no clear sense of eligibility or approval odds

they’re more likely to abandon halfway and seek a faster, if more expensive, alternative.

3. Personal Relationships and Human Guidance is Necessary

SMEs still value relationship managers and human guidance, even as they adopt digital channels. McKinsey’s analysis of SME banking notes that a digital-first approach with a personal touch is what moves the needle on satisfaction and share of wallet.

A flat, self-serve form that:

- doesn’t explain jargon (OD limits, DSCR, covenants),

- doesn’t offer real-time help, and

- goes silent after submission

Feels risky to business owners whose livelihood depends on that credit decision. Many would rather abandon than continue in a process they don’t fully understand or trust.

4. Perceived “Waste of Effort” is Higher

For a personal loan, losing 15 minutes to an abandoned journey feels annoying. For an SME owner who has already pulled bank statements, chased their accountant, and uploaded multiple PDFs, walking away mid-application means sunk costs in time and internal coordination. If they sense the lender is disorganized or slow, they’ll cut their losses early and try elsewhere.

Altogether, this creates multiple bottlenecks that a SME executive must pass through before they get a loan.

How Does the Complex SME Loan Journey Create Key Drop-Off Points?

Most SME journeys follow the same pattern:

- Awareness & Discovery – Marketing, referrals, or RM outreach.

- Pre-Qualification & Product Fit – Basic data capture and eligibility checks.

- Full Application & Data Capture – Detailed forms and declarations.

- KYC and Document Upload – Identity, business, and collateral proofs.

- Underwriting & Decisioning – Risk assessment, sometimes across multiple committees.

- Offer, Negotiation, Acceptance – Terms discussion and contract execution.

- Disbursal & Onboarding – Account setup, drawdown, and post-disbursal servicing.

At each stage of the SME loan journey, complexity creates specific drop-off hotspots:

- Early-Stage Confusion (Discovery → Pre-qualification): SMEs aren’t always sure whether they need a term loan, working capital line, or invoice finance, and product pages rarely explain the differences clearly. Many start the wrong application at this stage and abandon it as soon as requirements don’t match their expectations.

- Early-Stage Confusion (Discovery → Pre-qualification): This is where most loan application abandonment happens. Long forms, repeated data entry, slow or opaque KYC checks, and failed document uploads make the application stage feel endless. With every extra field and every unclear error message, SMEs are more likely to drop off.

- Late-Stage Silence (Underwriting → Offer): Even after a “complete” application, SMEs often face long underwriting cycles and little visibility into status. When the underwriting stage feels like a black box, many borrowers disengage or accept a faster offer from another lender instead of waiting.

- Channel Fragmentation (All Stages): SMEs move between website, app, call center, email, and branch. Without a unified journey view, each channel treats an SME as a new case, so a drop-off in one channel (for example, abandoning the app journey) is never “rescued” by proactive outreach from another (like an RM or contact center).

Loan application abandonment is common in digital lending because journeys are long, opaque, and high-friction by default. For SMEs, the combination of heavier documentation, tighter cash-flow timelines, and complex multistep journeys means they face more opportunities and stronger reasons to abandon than a typical retail borrower.

These bottlenecks can be eased by introducing real-time interventions that help customers get onboarded faster. We’ll take a look at how these interventions work in the next section.

How Can Real-Time Intervention Reduce SME Loan Application Abandonment?

At a high level, real-time intervention means noticing that a borrower is about to drop off while they are still in the journey and doing something useful about it.

Customer-journey orchestration platforms in banking use live behavioral signals (idle time, error events, page exits) plus profile data to trigger contextual messages and actions. Vendors consistently report that these real-time decisions cut abandonment and protect revenue, because they catch frustration before a customer gives up.

In lending specifically, journey observability tools show that when banks act on real-time journey data, they can reduce loan application drop-offs and improve satisfaction by fixing bottlenecks and nudging borrowers through the process.

On the back end, loan-origination automation and SME digital lending platforms are shortening decision times from weeks to days or even hours, precisely to shrink the window in which abandonment can occur. When you combine faster decisions with smart interventions at critical steps, you turn a leaky SME funnel into a guided path toward approval.

Real-time intervention is a design choice where you treat every stalled or struggling application as a “save opportunity”, powered by triggers and delivered through the right channels.

Let’s see how this works in a practical setting.

How Do You Design Real-Time Intervention Triggers Across the SME Loan Journey?

Real-time Interventions Start with Triggers (clear rules that say “when this happens in the journey, do that.”)

For SME loan application abandonment, you can design triggers around three dimensions:

- Behavioral triggers (what the SME is doing right now)

- Idle time: user sits on the “upload documents” step for 5+ minutes without progress.

- Repetitive actions: multiple validation errors on income or collateral fields.

- Exit signals: user scrolls to the end, doesn’t click “Next,” and closes the session.

Action examples:

- Show an inline tooltip (“You can upload a single PDF instead of 6 separate files”).

- Pop up contextual chat (“Need help with which GST returns to attach?”).

- Journey triggers (where they are in the funnel)

- Reached 70–80% completion but haven’t submitted within a defined time window.

- Completed application but KYC pending for more than 24 hours.

- Underwriting decision made but offer not viewed for two days.

Action examples:

- WhatsApp/SMS reminder with a deep link back to the exact step.

- Email summarizing what’s missing (“We’re only waiting for last 6 months of current account statements”).

- Value & risk triggers (who this SME is)

- High-value segment (ticket size, vintage, industry) stuck at any step.

- Risk models flag a strong applicant who suddenly drops activity.

Action examples:

- Push a task to the relationship manager to call within 2 hours.

- Route to a specialized support queue with full context.

A practical way to operationalize this is to build a small “trigger catalogue” for each stage of the SME journey:

- Trigger condition (e.g., “Application 60–90% complete, inactive 30 minutes”).

- Priority (e.g., “High – unsecured SME loan above ₹25L”).

- Intervention (e.g., WhatsApp reminder + in-app chat prompt).

- Owner & KPI (who monitors it; what uplift in completion you expect).

Tools that support real-time journey analytics and orchestration make this much easier, because they centralize events from web, app, and back-end systems and let you visually configure triggers and paths instead of hard-coding every rule.

This is also helpful because some channels are more likely to reduce abandonment rates than others.

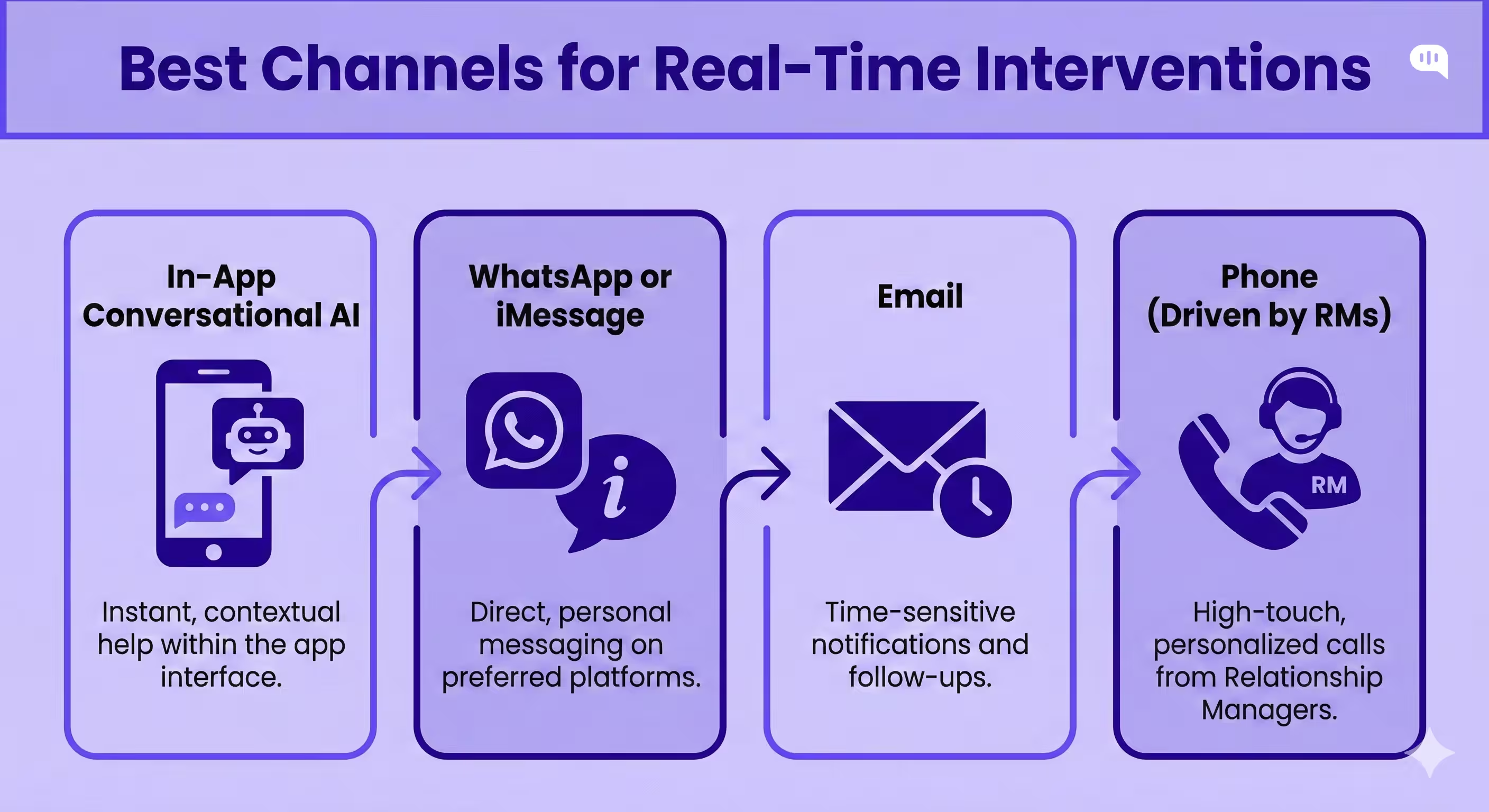

Which Intervention Channels Best Reduce SME Loan Application Abandonment?

Once you know when to intervene, the next question is where. Real-time decisions only move the needle if they land in a channel the SME actually sees and trusts.

Evidence from banking and fintech shows that conversational channels (chatbots, messaging apps, and guided conversational flows) are particularly effective at reducing onboarding and KYC abandonment, because they break complex tasks into smaller steps and provide instant clarification.

Meanwhile, AI-powered service chatbots reduce abandonment and support costs by handling repetitive queries, providing self-service, and routing complex issues to humans.

For SME loan applications, that translates into a simple playbook:

In-app / Web Chat & Conversational AI

- Ideal during form-fill and document steps.

- Guide SMEs through eligibility questions, document checklists, and jargon (“What exactly is DSCR?”).

- Triggered by behavioral signals (multiple errors, long idle time).

- Outcome: fewer mid-journey drop-offs because someone (or something) is “sitting next to them” explaining the process.

WhatsApp / SMS / Messaging

- Best for post-drop-off nudges and asynchronous document chasing.

- Suited for summary and documentation: sending checklists, offer details, or status updates when timing is less critical.

- Still useful as a backup channel, but slower than chat/messaging for real-time saves.

Phone & Relationship Managers

- Reserved for high-value or complex cases (secured loans, large working capital lines).

- Trigger conditions might include: large ticket size + stalled underwriting, or a valuable existing customer who’s been inactive on the application for several days.

- Outcome: RMs step in with full context, rather than making generic “just checking” calls.

The most effective SME lenders use real-time orchestration to pick the right combination based on value, risk, and customer preference. In practice, that might look like:

- Bot assist inside the journey

- WhatsApp if the SME drops off

- The RM calls only if the loan size and relationship value justify human time.

By combining smart triggers with channel-aware interventions, you give SMEs the nudge, clarity, or reassurance they need at exactly the moment they’re most likely to abandon.

This kind of automation is difficult because you need to build in observations into your product to trigger these interventions. But, data platforms and AI can help scale that use-case.

How Can Observability, Data, and AI Help You Detect Drop-Off Risk?

Most lenders don’t lose SME applications because they lack demand; they lose them because they can’t see where and when borrowers are about to give up.

Modern customer journey analytics and observability tools fix this by stitching together events across web, app, and back-end systems into a single, real-time view of the funnel. Banks use these platforms to map journeys, spot friction points, and see exactly where customers drop off during onboarding and loan applications. AI-powered observability then layers machine learning on top of these streams, detecting anomalies (for example, a spike in errors on the document-upload step) and flagging them before they cascade into widespread abandonment.

On the predictive side, the same techniques used for churn prediction in banking can be repurposed to estimate which applications are at highest risk of abandonment in the next few minutes or hours. That lets you move from static reports (“our abandonment rate was 60% last month”) to live decisions (“this high-value SME is stalling at 80% completion; trigger a WhatsApp nudge and alert the RM now”). In practice, observability, data, and AI work together as your early-warning system.

These tools will help you predict and design trigger-based systems. But next, you need to design a mechanism that actually supports your customers through the lending process.

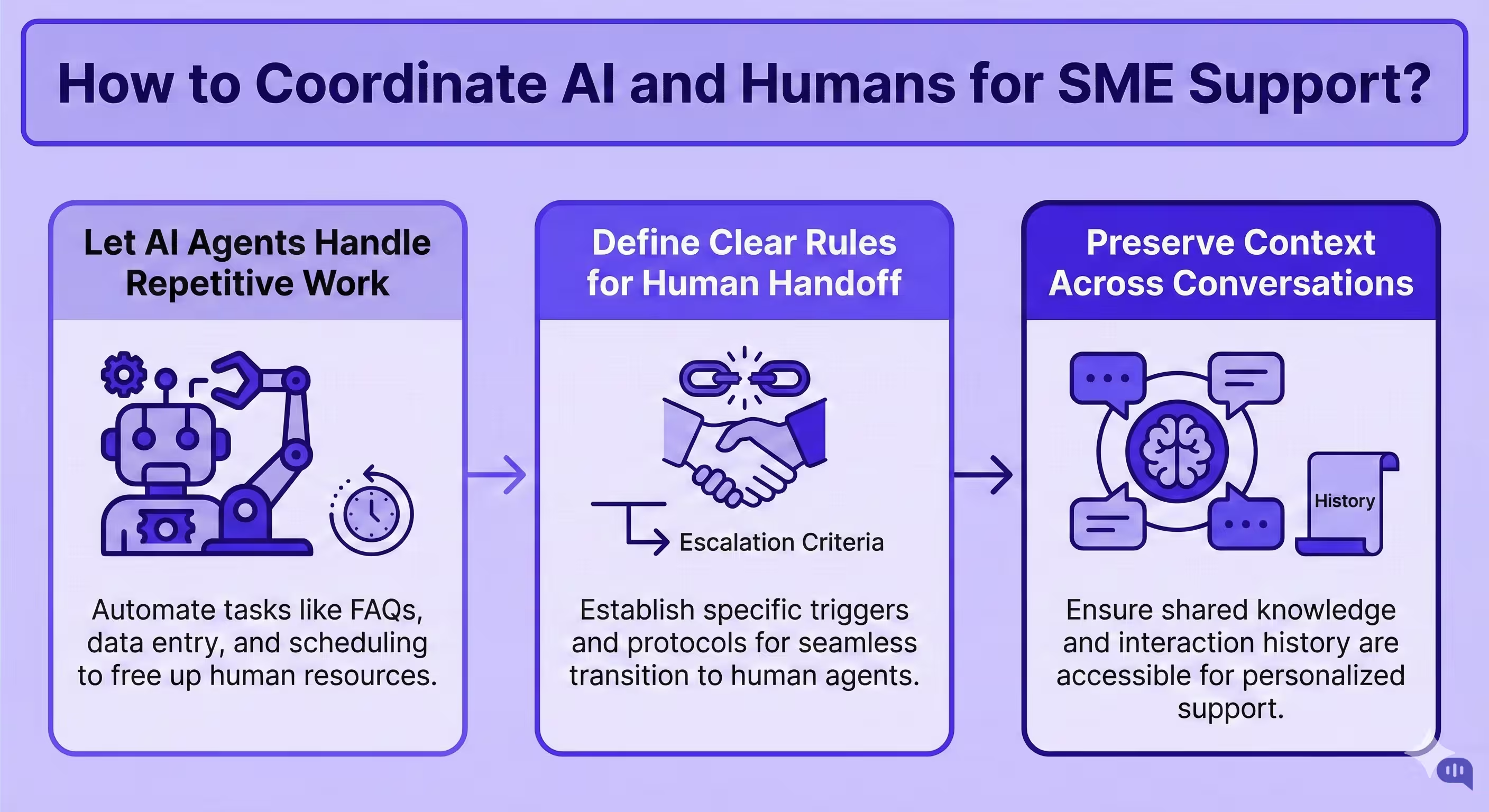

How Do You Coordinate Human and Digital Support for Complex SME Loan Cases?

For complex SME loans, the goal isn’t “bot or human,” it’s a coordinated front line where bots handle the routine, and humans step in exactly where judgment and nuance matter most.

Banks and SME lenders that get this right typically follow three principles:

- Let Digital Handle the Predictable, 24/7 Work: Banking and lending chatbots are now mature enough to handle eligibility questions, status checks, simple loan queries, and document checklists around the clock. This frees human teams to focus on higher-value, judgment-heavy cases.

- Define Clear Rules for Human Handoff: Best-practice guidance in financial services is very consistent: a good AI Agent must know when it has reached its limits and hand off seamlessly to a human agent, without making the customer repeat themselves.

In SME lending, that usually means escalating when:- Ticket size or client value crosses a threshold.

- The SME asks for negotiation, restructuring, or product comparison.

- The bot detects confusion (“I don’t understand,” repeated errors, high frustration signals).

- Preserve context across channels and teams: Research on chatbot–contact-center integration and “human handoff” stresses that the continuity of the conversation is what drives satisfaction: the customer should feel like they’re picking up where they left off, not starting from scratch.

Practically, that means:- Passing the full chat history, journey step, and document status to the RM or loan officer.

- Routing to the right team (SME underwriting, collections, RM desk) based on intent and product.

- Letting humans send the conversation back to the bot for repetitive follow-ups (e.g., document reminders).

In other words, digital support should filter, structure, and warm up SME cases, so humans work only on the subset where they add real value.

This is also where Kommunicate can help.

How Kommunicate Can Help Coordinate Human + Digital Support?

Kommunicate is built around exactly this bot + human hybrid model: AI agents handle the bulk of routine questions while providing a smooth, context-rich handoff to human agents when needed. Here’s how that maps to complex SME loan journeys:

AI Agents As the First Line of Support

- Use Kommunicate’s no-code AI agent builder to create bots that handle eligibility FAQs, document checklists, application status queries, and simple “what does this term mean?” questions across web, mobile, and in-app chat.

- Tie those bots into your SME knowledge sources (policies, product sheets, LOS help docs), so they can answer consistently without involving an RM for every basic query.

Smart, Configurable Human Handoff

- Kommunicate is specifically known for its human handoff capabilities: when the bot hits a limit, it routes the conversation to a live agent with full context, instead of forcing the SME to repeat their story.

Omnichannel SME Support (Especially WhatsApp)

Kommunicate plugs into WhatsApp as an official channel, so you can run the same AI agent + human team across web chat and WhatsApp—critical for SMEs who live on mobile.

This makes it easy to:

- Send real-time nudges when loan applications are abandoned mid-way.

- Let SMEs reply with documents, clarifications, or questions directly in WhatsApp, with agents stepping in when the bot escalates.

Integrations With Your Existing Stack

Kommunicate integrates with CRMs, helpdesks, and other systems (HubSpot, Freshdesk, Pipedrive, Zendesk, etc.), so chats and interventions can automatically become tickets, tasks, or deals for your credit and RM teams.

For SME lending, that means:

- A bot conversation about a stuck application can instantly create a “rescue” task for an RM with all context attached.

- RMs can see interaction history from web, app, and WhatsApp in one place.

Analytics on Where Humans vs. Bots Add the Most Value

Because Kommunicate tracks both bot and agent performance, you can see where in the SME loan journey humans are most frequently needed, and gradually push simpler cases back to automation. This keeps humans focused on complex loans and distressed cases.

So, how can you implement Kommunicate and customer journey analytics into your app or website? Let’s explore a basic 90-day implementation plan next.

How Can SME Lenders Implement Real-Time Interventions in 60–90 Days?

We’re going to target a 60-90 day implementation. To help you achieve this, we’re going to get cues from LOS/digital lending implementation timelines (6–12 weeks) and journey orchestration rollouts that target a 60–90-day windows.

| Phase & Timeline | Goal | Key Actions | Primary Owners | Example Deliverables |

| Weeks 1–2 – Discover & Baseline | Understand current SME funnels and quantify loan application abandonment | – Map existing SME loan journeys (web, app, RM, branch) – Pull 6–12 months of funnel data: started vs. submitted vs. approved – Identify top 3–5 drop-off steps (e.g., docs, KYC, underwriting wait) – Define success metrics (target reduction in abandonment, uplift in completions) | Product owner, credit ops, analytics, IT | – Current-state journey maps – Baseline abandonment KPIs by step and channel – 1–2 page “problem statement” + target metrics |

| Weeks 3–4 – Design Triggers & Interventions | Decide when and how to intervene in real time | – For each key drop-off point, define 1–2 behavioral/ journey triggers (e.g., idle 5 mins at docs; 80% complete but no submit) – Map interventions to channels: in-app chat, WhatsApp/SMS, email, RM call – Draft message templates and escalation rules (when to push to human agent/RM) – Prioritize by impact (loan value × abandonment rate × ease) | Product, CX, contact center / RM leadership | – Trigger catalogue (conditions, channel, owner, KPI) – Message + playbook library for bots, agents, and RMs – Short design doc for real-time orchestration rules |

| Weeks 5–8 – Integrate Data & Configure Tooling | Connect data sources and set up real-time orchestration | – Choose / configure journey analytics & orchestration tool (or enhance existing stack) – Integrate web & app events, LOS/CRM data, and basic risk/segment flags – Connect channels (chat widget, WhatsApp API, email, Contact-center routing) – Configure the priority triggers and flows in the tool’s UI (no/low-code where possible) | IT/engineering, architecture, vendor team, data/analytics | – Live event stream for SME application journeys – Orchestration flows configured for 3–5 critical triggers – Staging environment with end-to-end test journeys |

| Weeks 9–10 – Pilot & Optimize on One SME Product | Prove impact on a contained segment before scaling | – Run a controlled pilot on one SME product (e.g., unsecured WC loans) or region – Enable a subset of triggers and channels only (focus on 2–3 highest-impact saves) – Monitor real-time dashboards for completion rates and response to interventions – A/B test with control group (no interventions) to measure uplift | Product, analytics, risk, front-line ops | – Pilot report showing change in abandonment, completion, and time-to-decision – Refined trigger logic and message variants – Go/no-go decision + scale-up plan |

| Weeks 11–13 (up to 90 days) – Scale & Embed Operations | Industrialize real-time interventions across SME lending | – Add triggers and orchestration to more SME products / channels – Train agents and RMs on new workflows, dashboard, and escalation rules – Formalize governance: who owns trigger catalogue, experiments, and KPIs – Bake metrics into monthly business reviews (abandonment, rescued apps, incremental funded volume) | Business leadership, CX, risk, training/HR | – Full rollout plan and updated SOPs – Playbooks for agents/RMs handling “rescued” applications – Ongoing experimentation roadmap for new triggers and AI models |

This blueprint gives you a controlled way to change borrower behavior at specific drop-off points and prove that real-time interventions actually move the needle. But a blueprint is only as good as the feedback loop around it. The next step is to define how you’ll track rescued applications, uplift in completion rates, and incremental funded volume versus a clean control group. In other words: once you’ve wired in triggers and channels, how should you measure the impact of your loan application abandonment strategy?

How Should You Measure the Impact of Your Loan Application Abandonment Strategy?

Once you’ve wired in real-time triggers and interventions, the hard question is simple: did it actually change borrower behavior and funded loans, or just add noise?

Banks and lenders that actively manage loan application abandonment usually track a mix of funnel KPIs, intervention KPIs, and business KPIs. Industry guidance on digital onboarding and lending optimization keeps coming back to the same themes: measure completion rates at each step, monitor drop-offs where friction is highest (forms, KYC, documents), and tie any uplift back to approved and funded accounts, not just clicks.

Here’s a concise KPI set you can use:

- Start-to-Submit Conversion Rate – Percentage of SME borrowers who start a digital application and successfully submit it. This is the core “loan application abandonment” KPI; a rising completion rate here shows your journey and real-time saves are working.

- Step-Level Drop-Off Rate – Abandonment percentage at key stages (e.g., product selection, application form, KYC, document upload, underwriting wait). Digital onboarding benchmarks recommend zooming in at step level to see exactly where friction and abandonment concentrate.

- Rescued Application Rate – Share of applications that were abandoned or idle and then completed after an intervention (chat prompt, WhatsApp nudge, RM call). This tells you whether real-time interventions are actually saving deals or just pinging people.

- Submit-to-Approval Conversion Rate – Percentage of submitted SME applications that receive an approval. While not purely “abandonment,” it’s important to separate funnel losses due to drop-off from those due to credit policy and risk decisions.

- Incremental Funded Loan Volume vs. Control – Additional funded amount (or number of booked loans) attributable to interventions when compared against a control group with no interventions. Lenders and journey optimization platforms often use A/B tests to prove financial impact in exactly this way.

- Time to Completion & Time to Decision – Median time from application start to submission, and from submission to credit decision. Industry analyses show that reducing time to decision is tightly correlated with lower abandonment, especially for SMEs under cash-flow pressure.

- Channel-Level Engagement & Completion – How different channels (web, app, chat, WhatsApp, RM calls) contribute to rescued applications and completed journeys. This helps you see where interventions are most effective and where you’re overspending for little uplift.

Measuring impact is only half the story. Every new trigger, data feed, and outreach channel also changes your risk and compliance surface area, from how you capture consent for WhatsApp nudges to how you store behavioral data and govern AI models.

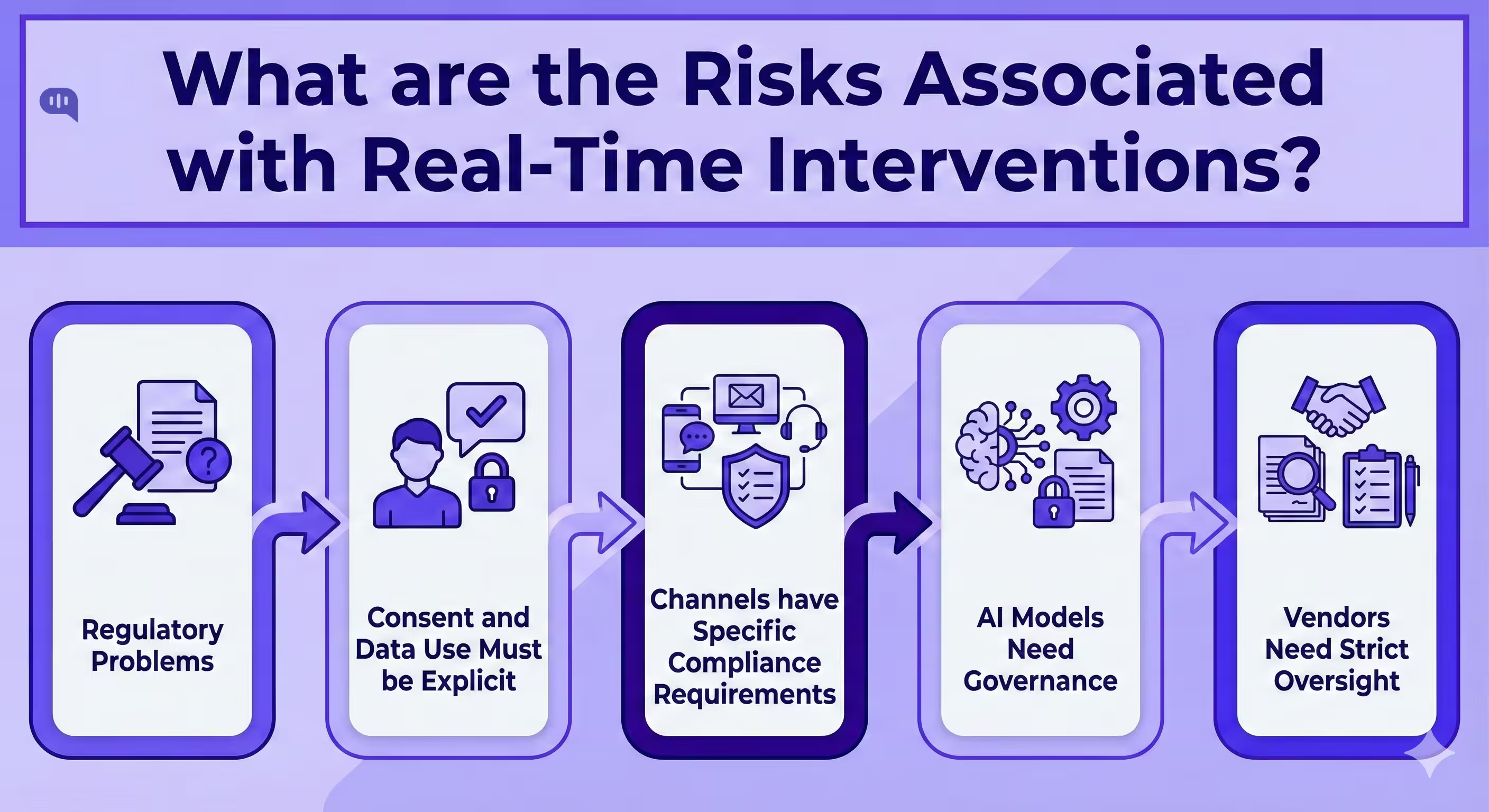

How Do Risk, Compliance, and Customer Consent Shape Real-Time Interventions?

Real-time interventions are powerful precisely because they sit at the intersection of behavioral data, automated decisioning, and proactive outreach. That also means they sit right in the crosshairs of regulators. Digital lending rules, data-protection laws, and emerging AI/algorithm guidance all converge on the same themes: collect less data, be explicit about how you use it, get (and respect) consent, and keep humans in the loop when decisions are high-impact.

- Interventions Sit in a Regulated Zone: Real-time nudges rely on behavioral data, automated logic, and proactive outreach, so they must comply with digital lending, data-protection, and AI rules (data minimization, transparency, human oversight).

- Consent and Data Use Must Be Explicit: Frameworks like RBI’s digital lending guidelines and data-protection laws require need-based data collection, clear consent for using that data, and easy ways for borrowers to revoke consent or opt out of communications.

- Channels are a Compliance Choice, not just UX: Using WhatsApp, SMS, or email for rescue nudges is only acceptable when you have documented opt-in, honor opt-outs, cap frequency, and follow telecom and platform policies on what you’re allowed to send.

- AI Models Need Governance and Explainability: Any model that scores abandonment risk, prioritizes SMEs, or influences loan outcomes must sit under model-risk management with documentation, bias checks, and the option for humans to review and override decisions.

- Vendors Must be Under Strict Oversight: Journey analytics, orchestration, and conversational AI providers have to operate under your contracts, DPAs, and security standards, with limited data access and full audit trails for triggers and interventions.

Conclusion

Loan application abandonment is a structural leak in SME lending economics. When 60–70% of digital applications never make it to submission, you’re not just losing leads, you’re burning marketing budgets, underutilizing underwriting capacity, and leaving profitable SME relationships on the table. The path forward is an operating model where observability, real-time triggers, and coordinated human + digital support work together: you detect the exact moments SMEs struggle, intervene through the right channel, and guide them to a decision with clarity on requirements, timelines, and next steps.

If you get this right, your loan funnels stop behaving like a sieve and starts looking like a guided journey—shorter time-to-decision, higher completion and approval rates, and RMs focused on the cases where they truly add value. That’s exactly the layer Kommunicate is built to power: AI agents that handle repetitive journey queries, smart routing and handoff to humans, and orchestration across web and WhatsApp so you can “rescue” more applications without overwhelming your teams. If you’d like to see how this could work on your SME lending stack, you can book a demo with Kommunicate here