Updated on May 18, 2026

Your marketing team is filling the top of the funnel. Prospects are requesting quotes. And then — nothing.

The insurance industry has the highest “cart abandonment” rate among sectors. Roughly 84% of prospects who start a quote never complete it, and even among those who receive a quote, the average conversion to a bound policy ranges from 10% to 20%. For most carriers, that means you’re converting one out of every ten interested prospects on a good day.

This is a process problem. The friction in how quotes are captured, delivered, and followed up on is bleeding revenue at every stage. And the carriers pulling ahead right now are solving it with conversational AI.

This guide breaks down exactly where the leaks are and how conversational AI fixes them. We’re going to cover:

- Why don’t quotes convert?

- What does conversational AI do differently?

- The playbook – Conversational AI at each stage of the funnel

- Underwriting speed as a conversion lever

- How to measure the efficacy of conversational AI interventions?

- Challenges and problems to watch out for

- Conclusion

- FAQs

Why don’t quotes convert?

Before reaching for a solution, it’s worth being precise about the problem. Quote abandonment has several distinct causes, each requiring different interventions.

- Form friction and cognitive overload. Traditional online quote forms ask prospects to answer 20–40 fields before they see any value in return. The moment a user hits a question they find confusing or intrusive, they leave. Studies consistently put online form abandonment rates for insurance at 60–80%.

- Slow follow-up. Leads go cold fast. A prospect who requested a quote at 9 PM on Tuesday and hasn’t heard from anyone by Wednesday afternoon has already moved on, or worse, gotten a call from a competitor. Speed to lead is not a nice-to-have. The insurer who responds first wins the bind far more often than the one with the slightly better price.

- One-size-fits-all outreach. Most follow-up sequences treat all quoted-not-sold prospects identically. But the person who dropped off because the form was confusing is different from the one who got busy, and from the one who’s still comparing options. Undifferentiated outreach converts none of them effectively.

- Disconnected systems. CRM, agency management system, comparative raters, and email tools often don’t sync properly. The result is a follow-up that falls through the cracks during shift changes, high-volume periods, or when a producer leaves.

- The psychology of “quoted not sold.” A significant share of people who request quotes aren’t ready to buy. The mistake is treating them as lost rather than as prospects in a longer nurture cycle. Most carriers don’t have a disciplined re-engagement strategy for this segment.

While conversational AI for insurance is not a silver bullet for any of these problems, it can have a positive effect on most of them.

What does conversational AI do differently?

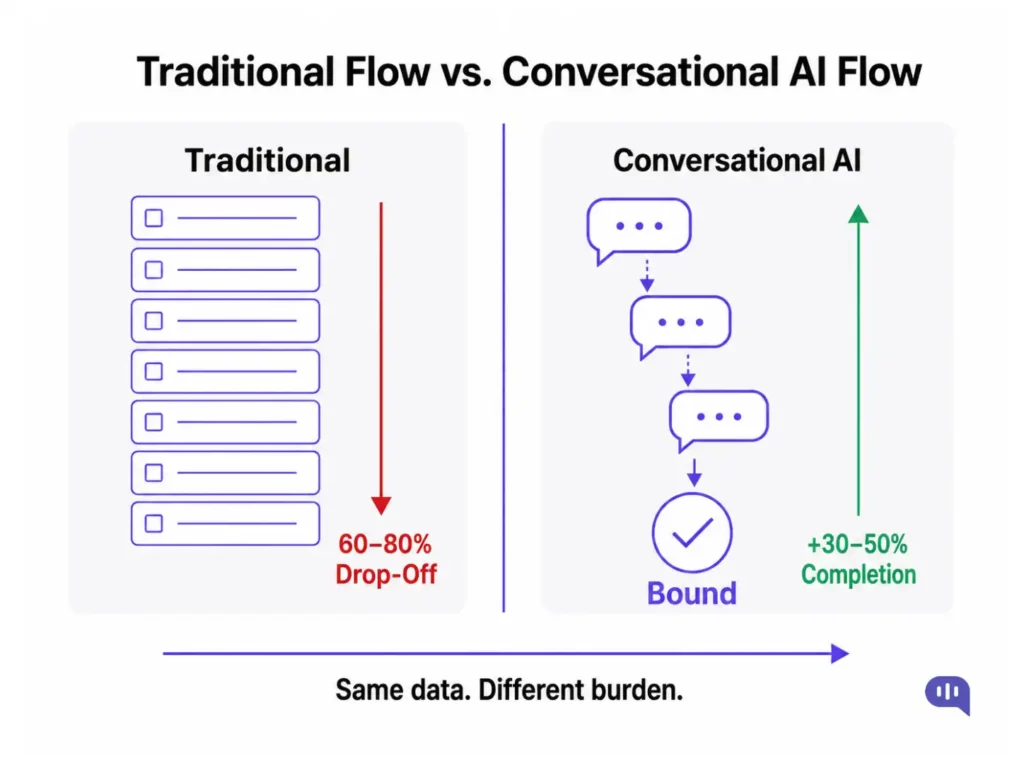

Conversational AI doesn’t just speed up the existing process. It restructures it.

The table below maps the same journey (prospect to bound policy) under a traditional model versus a conversational AI model. The steps are identical. What changes is who does the work, how long each step takes, and how many prospects drop off before the next one comes in.

| Stage | Traditional Flow | Conversational AI Flow | Impact |

|---|---|---|---|

| Initial Contact | Prospect lands on a 20–40 field web form | AI agent opens with one question: “What type of coverage are you looking for?” | Abandonment drops from 60–80% to 30–50% |

| Data Collection | Prospect fills all fields upfront, regardless of relevance | Agent asks questions dynamically based on prior answers; irrelevant fields never appear | Cleaner data, higher completion, shorter time-on-page |

| Data Validation | Errors caught by the underwriter days later, triggering back-and-forth | Agent detects incomplete or inconsistent answers in real time and prompts for clarification | Underwriters receive complete submissions; cycle time shrinks |

| Quote Delivery | Prospect submits form and is told, “We’ll be in touch.” | Eligible risks receive an indicative price within the same conversation | Prospect stays engaged while intent is highest |

| Follow-Up | Producer calls or emails the next business day, or doesn’t | AI triggers a personalized follow-up sequence within minutes, segmented by behavior | Response time goes from hours or days to under five minutes |

| Lead Routing | The producer manually reviews and assigns to the right queue | AI delivers a structured summary and routes automatically by coverage type, risk profile, and territory | No leads fall through shift changes or producer turnover |

| Quoted-Not-Sold | Prospect is rarely re-engaged systematically | AI runs a 30/60/90-day re-engagement sequence based on behavioral signals | Recovers business from warm prospects already in the database |

| Underwriter Handoff | Underwriter receives a partial email chain or unstructured PDF | Underwriter receives a clean, normalized file with all required fields populated | Submissions processed faster; quote capacity increases |

The structural shift is this:

- In the traditional model, the prospect carries most of the burden.

- In the conversational AI model, the system carries that burden.

The prospect answers one question at a time and gets a response before they leave.

For a carrier processing 5,000 monthly website visitors, moving from a 20% form completion rate to a 40% conversation completion rate translates to over 1,000 additional qualified quote requests per month.

The structural advantages of using conversational AI for optimizing conversions

Beyond completion rates, conversational AI creates three structural advantages:

- Instant responses. AI agents capture and qualify quote requests at 10 pm or 6 am with no degradation in quality or consistency. Every lead is engaged immediately, not when a producer gets to their inbox the next morning.

- Dynamic conversation flows. Unlike static forms, AI agents adjust their questions based on previous answers. A prospect seeking commercial auto coverage sees a completely different conversation path than one shopping for workers’ comp. This keeps interactions relevant and data quality high.

- Compression of the intent-to-commitment gap. A quoting process that begins and ends inside a single conversation removes friction between the moment a prospect decides they want coverage and the moment they can act on it.

If you want to bring these advantages into your organization, you need to follow a solid playbook for implementation.

The playbook – Conversational AI at each stage of the funnel

Top of funnel: Replace form abandonment with conversation completion

- The implementation. Deploy a conversational AI agent on your website, landing pages, and high-intent channels like WhatsApp. Configure it to handle your lines of business with distinct conversation flows for each coverage type.

- What to build. The agent should open with a single, low-friction question (“What type of coverage are you looking for?”) and guide the prospect through data collection step by step. It should detect incomplete or inconsistent data in real time and ask for clarification before the conversation ends.

- Integration priority. Connect the agent to your quote API so eligible risks receive an indicative price within the same conversation. Prospects who can see a number before they leave are far more likely to convert than those who are told, “We’ll be in touch.”

- Metrics to set before launch. Baseline your current form completion rate, average time-to-first-quote, and cost per completed quote request. These are your benchmarks.

Mid-Funnel: Fix Speed to Lead and Personalize Follow-Up

- The implementation. For prospects who complete a conversation but don’t bind immediately, AI should trigger a follow-up sequence within minutes. The sequence should be differentiated by what you know: coverage type, risk profile, where they dropped off, and whether they were shown a price.

- What to build. Segment your quoted-not-sold pool into at least three buckets: prospects who saw a price and didn’t proceed (likely shopping around), prospects who completed data collection but haven’t received a quote (operational gap), and prospects who dropped off mid-conversation (friction or not-ready-to-buy). Each segment gets a different re-engagement flow.

- The speed-to-lead rule. Set a policy that no qualified prospect waits more than five minutes for a response during business hours and no more than eight hours outside of them. AI handles the immediate response; your producers handle the follow-through. Tools like Retell AI have documented data intake call times dropping from nine minutes to roughly six minutes by automating the structured data-collection portion of the call, freeing producers to spend that time on the consultative sale.

- Metrics to watch. Track lead response time, open and reply rates by segment, and conversion rate from quoted-not-sold to bound, broken out by follow-up sequence.

Bottom of Funnel: Route, Qualify, and Reduce Submission Friction

- The implementation. Qualified leads should route automatically to the right producer, underwriter, or service team based on coverage type, risk profile, and territory. The AI agent should deliver a structured summary with every handoff.

- What to build. Define routing rules upfront. A small commercial account goes to a different queue than a mid-market risk. A prospect who’s been quoted and re-engaged twice is a higher priority than a fresh inbound. Build your routing logic around those distinctions.

- For underwriting teams. Conversational AI also addresses the bottleneck in submission intake. Natural language processing can extract and normalize data from web forms, emails, broker submissions, and PDFs. This is where the most dramatic reductions in cycle time occur.

- Metrics to watch. Submission completeness rate, time from first contact to quoted, and underwriter quote capacity (how many submissions per underwriter per week).

Post-Quote: Build a Re-Engagement Engine for Quoted-Not-Sold

This is the most underbuilt part of most carriers’ funnels. Prospects who received a quote but didn’t bind are warm leads. They’ve already done the work of providing their information. The question is whether you have a systematic way to stay in front of them.

- What to build. A 30/60/90-day re-engagement sequence for quoted-not-sold prospects, personalized by line of business, original quote date, and any behavioral signals (did they open the quote email? Did they return to your website?). AI should trigger re-engagement automatically, with producers brought in only when a prospect signals renewed interest.

We’ve helped insurance carriers deploy this systematically. The report meaningful recovery of business that would otherwise have lapsed permanently.

The economics are straightforward: you’ve already paid to acquire the lead. Re-engagement costs are a fraction of new acquisition costs.

Another facet of conversion that is often ignored includes underwriting. We’ll briefly cover that next.

Underwriting speed as a conversion lever

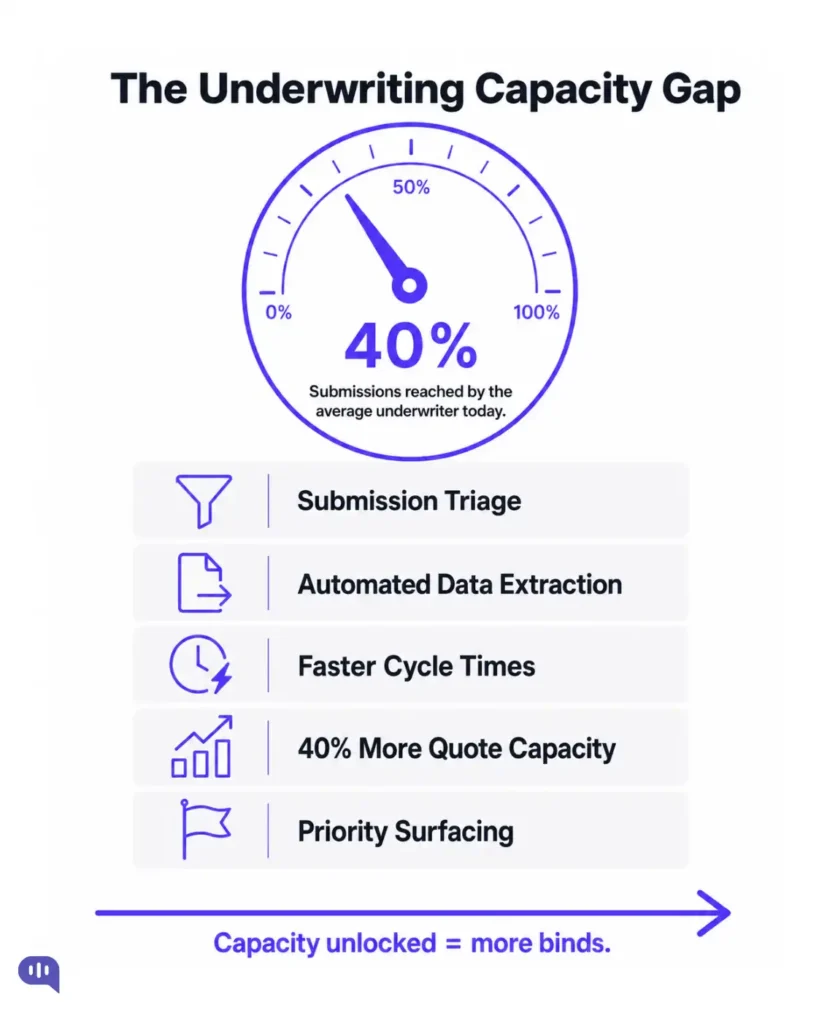

CROs often focus the conversion conversation on sales and marketing. For commercial lines and specialty risks, the underwriting cycle is itself a major conversion lever, and it’s the one most carriers are leaving untouched.

The core problem is capacity, not quality. The average underwriter today reaches only about 40% of the submissions on their desk because there aren’t enough hours in the day. AI changes that math directly:

- Submission triage. Machine learning models rank incoming submissions against underwriting appetite, risk profile, and historical conversion rates, so your team works the highest-probability opportunities first, not whatever landed at the top of the inbox.

- Automated data extraction. NLP pulls and normalizes data from emails, PDFs, broker portals, and web forms, so underwriters open a clean, structured file instead of a partially complete email chain.

- Faster cycle times. Brokers stop shopping elsewhere when you quote first.

- Better capacity utilization. With administrative work automated, underwriters spend more time on the complex judgment calls that actually require their expertise. Carriers with mature AI underwriting deployments are reporting 40% increases in quote capacity and combined ratios that are seven to ten points better than industry averages.

- Priority surfacing. High-probability submissions that might otherwise sit in a queue get flagged and actioned within hours, concentrating your team’s limited capacity where it generates the most bound premium.

For executives deciding where to invest first, underwriting workflow automation often delivers faster and more measurable ROI than consumer-facing tooling. Once you’ve built the conversion infrastructure within the funnel, the following section covers how to determine whether any of it is actually working.

Once you implement these interventions, it’s critical to measure some metrics that specifically trace their efficacy.

How to measure the efficacy of these conversational AI interventions?

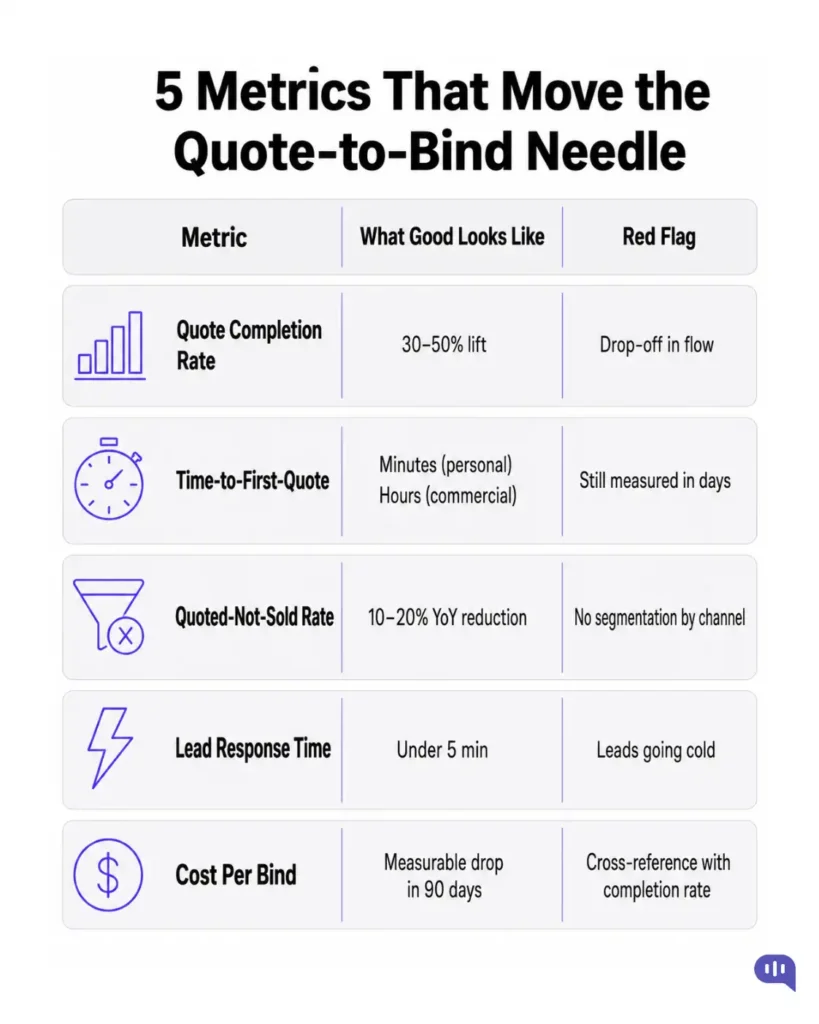

Conversational AI creates more data than most carriers are used to having. The risk is tracking everything and understanding nothing. These are the metrics that actually correlate with improved quote-to-bind rates:

| Metric | What It Measures | What Good Looks Like | What a Bad Number Tells You |

|---|---|---|---|

| Quote Completion Rate | % of quote conversations that result in a complete data submission | 30–50% lift over your pre-AI web form baseline | Top-of-funnel friction — the conversation flow has a drop-off point that needs to be identified and fixed |

| Time-to-First-Quote | Time from first contact to a prospect receiving a price | Minutes for personal lines; hours for commercial lines | You’re losing binds to whoever quotes fastest — brokers and consumers don’t wait |

| Quoted-Not-Sold Rate | % of prospects who received a quote but didn’t bind, inverse of your conversion rate | Track as a baseline, then reduce by 10–20% year-over-year | Variance by line of business, channel, or producer tells you exactly where the leak is concentrated |

| Lead Response Time | Time from conversation completion to first human or AI follow-up | Under 5 minutes during business hours; under 8 hours outside them | Your follow-up infrastructure isn’t keeping pace with intake — leads are going cold before anyone touches them |

| Cost per Bind | All-in acquisition cost divided by bound policies | Measurable reduction within 90 days of AI deployment | Either acquisition spend is too high or conversion rates are too low — the metric doesn’t distinguish, so cross-reference with completion rate |

Set a 90-day review cadence for the above metrics. Conversation flow optimization is where most of the long-term conversion gain comes from.

Challenges and problems to watch out for

Conversational AI in insurance has clear ROI, but implementation failures are common. Here’s what to get right.

- Don’t automate the wrong moments. AI excels at structured data collection, routing, and follow-up. It is not a replacement for a producer in a complex coverage conversation. Define your handoff triggers clearly: a prospect who’s asked three clarifying questions about coverage scope, or a commercial risk above a certain premium threshold, should talk to a human. Automate the process around the expert, not instead of them.

- Data quality determines everything downstream. The accuracy of quotes, routing decisions, and underwriting risk assessment all depend on clean intake data. Build data validation into the conversation flow, not as a post-processing step.

- Compliance is non-negotiable. State licensing, disclosure, and data-handling requirements vary significantly. Ensure your conversational AI deployment is reviewed for compliance in every market you operate. What a prospect says to an AI agent during a quote conversation may have legal implications for the policy.

- Pilot before you scale. Only 22% of insurers have successfully scaled AI beyond pilot programs. The failure mode is almost always the same: a promising pilot is deployed broadly before the integration work, change management, and data infrastructure are ready. Start with one line of business or one channel. Prove the metrics. Then expand.

Conclusion

Quote-to-bind improvement is not a single lever. It’s the cumulative effect of reducing friction at intake, responding faster, following up smarter, routing more precisely, and re-engaging prospects who would otherwise disappear.

Conversational AI addresses all of these simultaneously. The underwriting teams, producers, and service staff working alongside these systems become more effective over time, not just more efficient.

The carriers building this infrastructure now are compounding an advantage that will be difficult for late movers to close. The window to implement and optimize ahead of the market is open, but it narrows as more carriers reach production deployment.

The practical starting point: pick the single biggest leak in your funnel and deploy a focused AI solution against it. Measure over 90 days. Build from there.

If you need help automating this process, feel free to book a call.

FAQs

The quote-to-bind rate is the percentage of prospects who receive a quote and subsequently purchase a policy. Industry-wide, this ranges from 10% to 20% for most carriers. High-performing carriers with mature digital and AI capabilities achieve 25–30% or higher in personal lines. Commercial lines tend to be lower due to longer sales cycles and the involvement of brokers. If you don’t know your current rate by line of business and channel, that’s the first thing to fix.

A standard chatbot follows a rigid script and breaks the moment a user goes off-path. Conversational AI uses natural language processing to understand intent, handle variation in how people phrase things, and dynamically adjust the conversation based on prior answers. In a quoting context, that means it can handle “I need coverage for my delivery vans” the same way it handles “commercial auto for a fleet of five vehicles,” and route both correctly without requiring exact phrasing.

The practical difference is completion rate: scripted chatbots tend to frustrate users; well-designed conversational AI agents guide them through.

No, and implementations that try to use it that way tend to fail. The strongest deployments use AI to handle the structured, repetitive work (data collection, routing, initial follow-up, submission intake) so that producers and underwriters can spend more time on the judgment-intensive work that actually requires their expertise.

Carriers reporting 40% increases in underwriter quote capacity aren’t doing so by reducing headcount; they’re doing so by removing the administrative load that consumed most of their team’s time.

The fastest wins typically come from fixing quote form abandonment at the top of the funnel and implementing a quoted-not-sold re-engagement sequence. Both have short implementation cycles, clear before/after metrics, and work on leads you’ve already paid to acquire.

Underwriting workflow automation delivers a larger ROI but takes longer to implement and measure. For a 90-day proof-of-concept, start with one channel and one line of business, set a baseline for completion rate before launch, and measure the delta at 30/60/90 days.

This varies by state and line of business, but the core requirements are consistent: any AI system collecting prospect information for insurance quoting purposes must include appropriate disclosures, handle personally identifiable information in accordance with state privacy laws, and ensure that any coverage representations are reviewed for accuracy.

Your compliance and legal teams should review conversation flows before deployment. The good news is that AI creates a complete audit trail of every interaction, which is better than the inconsistent documentation from unstructured producer calls.

A focused deployment typically takes six to twelve weeks from scoping to live. Broader deployments across multiple lines, channels, and back-end systems take longer and should be phased. The common mistake is underestimating the integration work: the conversational AI layer itself deploys quickly, but connecting it cleanly to your quoting engine, routing rules, and CRM is where projects stall. Budget for integration time as a first-class project cost.

Five things matter most: insurance domain training (generic AI tools perform poorly on coverage-specific terminology and edge cases), real-time quote API integration, compliance framework coverage across your operating states, depth of CRM and AMS integration, and conversation analytics that feed a continuous optimization loop.

A vendor who can show you a live conversation flow and the analytics dashboard behind it is ahead of one who can only show you a pitch deck.