Updated on July 6, 2026

TL;DR

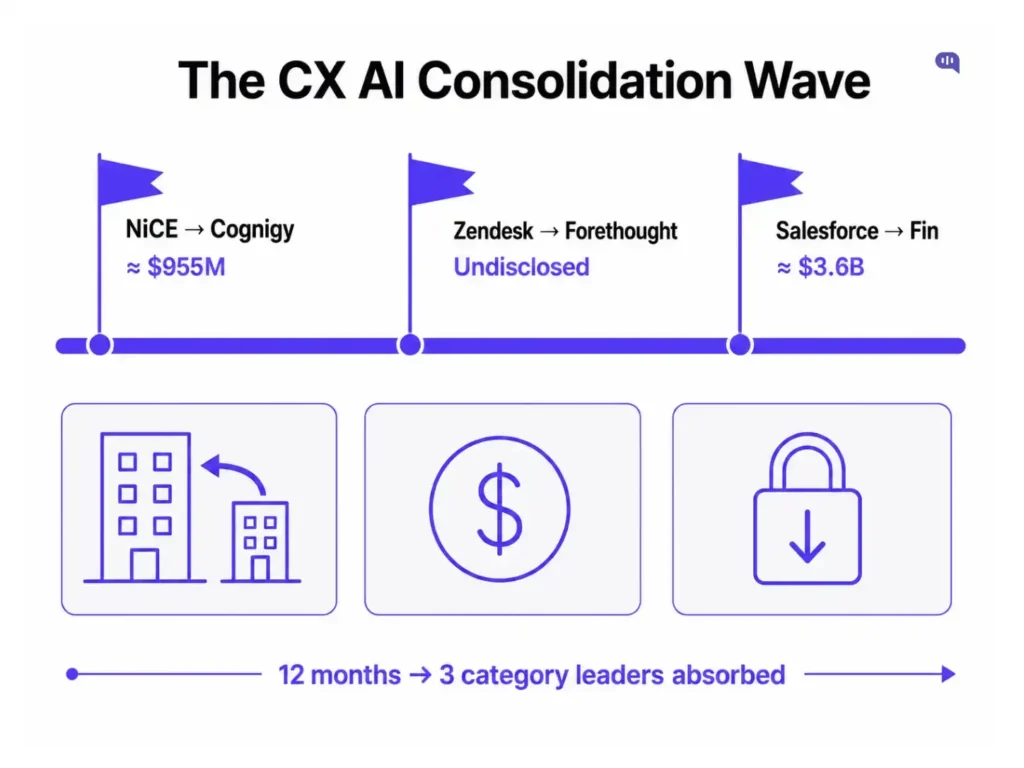

The AI customer support market is consolidating, with three large acquisitions in the past year:

- NiCE acquired Cognigy

- Zendesk acquired Forethought

- Salesforce acquired Fin(Intercom)

Enterprises that built their support infrastructure around a single independent vendor face pricing pressure and reduced leverage at renewal. The solution is not running multiple platforms in production simultaneously. It is maintaining active POCs and acquisition-proof contracts across a medium time horizon, so you always have a credible alternative in the queue.

The customer support AI market just got a lot more interesting, and not in the way most enterprises planned for.

- In June 2026, Salesforce agreed to acquire Fin (formerly Intercom) for approximately $3.6 billion.

- Nine months earlier, NiCE had closed its $955 million acquisition of Cognigy, absorbing one of the leading enterprise conversational AI platforms into its CXone stack.

- In March 2026, Zendesk acquired Forethought, pulling its AI triage and autonomous resolution capabilities into the Zendesk product.

These signals point to the start of structural consolidation in customer support AI, and enterprises that built their support infrastructure around a single independent vendor are beginning to feel the implications for their options.

This article makes a specific argument: enterprises running customer support on AI do not need to deploy multiple vendor tools simultaneously in production. But they do need an active, ongoing procurement posture that keeps alternatives warm and proof-of-concepts running across a medium time horizon. We’re going to talk about:

- The consolidation wave in CX AI

- The two problems consolidation creates

- What does vendor diversification actually mean?

- How to build a competitive advantage during consolidation?

- What enterprises should actually do: A 90-day implementation plan

- How can Kommunicate help?

The Consolidation Wave in CX AI

The table below covers the three major CX-specific acquisitions completed between mid-2025 and mid-2026. In each case, a large platform company acquires a category-leading independent to close a capability gap, rather than building from scratch.

| Acquisition | Closed | Deal Size | What the Acquirer Got | What Standalone Customers Face |

|---|---|---|---|---|

| NiCE acquires Cognigy | September 2025 | ~$955M (approx. 25x 2024 revenue) | Enterprise conversational and agentic AI across voice and chat; 1,000+ brands including Bosch, Lufthansa, Mercedes-Benz | NiCE’s CXone platform strategy now governs Cognigy’s roadmap and pricing |

| Zendesk acquires Forethought | March 2026 | Undisclosed | AI triage, autonomous resolution, and agent assist capabilities | Forethought’s standalone contracts transferred to Zendesk’s commercial team |

| Salesforce acquires Fin (formerly Intercom) | Pending close, FY2027 Q4 | ~$3.6B | 30,000+ business customers; Fin AI agent built for full-conversation resolution across chat, email, voice, WhatsApp | Too early to call |

Three independent AI support vendors have been absorbed into larger platform companies. In each case, the acquirer paid a significant premium for the capability rather than building it. In each case, existing customers found their commercial and product relationship had changed without their input.

The pattern will continue, and every independent AI support vendor that reaches meaningful scale becomes a candidate for the same move. And that can be a problem for the end users.

The two problems consolidation creates

1. AI agents now cost significantly more

Modern AI agents are substantially more capable than their predecessors two years ago. They resolve:

- Complex multi-turn conversations

- Integrate with CRMs

- Handle voice and async channels simultaneously

- Escalate with context intact

But, a pricing jump has also predictably followed this capability jump.

When an AI support vendor gets acquired by a larger platform company, the economics shift in predictable ways. The acquirer needs to justify the purchase price, integration work, and ongoing R&D. The fastest lever is pricing. A platform that charges per resolution or per seat under independent ownership is repriced within a broader enterprise suite, bundled with capabilities the customer may not need, and structured around the acquirer’s commercial model rather than the customer’s support workflow.

The NiCE-Cognigy deal followed this logic. Cognigy had over 1,000 enterprise customers across voice and chat channels. NiCE paid approximately 25 times Cognigy’s 2024 revenue to acquire it, a multiple that signals strategic necessity rather than financial efficiency. Industry analyst commentary at the time described the deal as “the beginning of an industry move to streamline the total number of contact center applications.” That streamlining happens on the acquirer’s terms.

This is how acquisitions work.

2. A single-vendor stack has no pricing floor

The deeper structural problem is what a Zapier survey published in early 2026 found: only 6% of enterprise leaders said they could switch AI vendors without material disruption. That number reflects years of deepening integration, custom workflow dependencies, and proprietary data that lives inside one vendor’s infrastructure.

When 94% of your peers cannot leave, you have no leverage in a renewal negotiation. The vendor knows this. Pricing in that environment reflects it.

Enterprise AI architect Kai Waehner mapped this dynamic in an April 2026 analysis: “Enterprises that build their agentic workflows on proprietary orchestration layers find that lock-in compounds at every layer of the stack.”

The same analysis found that the enterprise LLM market had already become significantly concentrated, with the leading provider holding approximately 40% of enterprise API spend. The distribution shifts quarter to quarter, but the underlying dynamic of concentration risk remains constant regardless of which provider leads.

To avoid vendor lock-in and sudden price increases, companies need to diversify their vendor list.

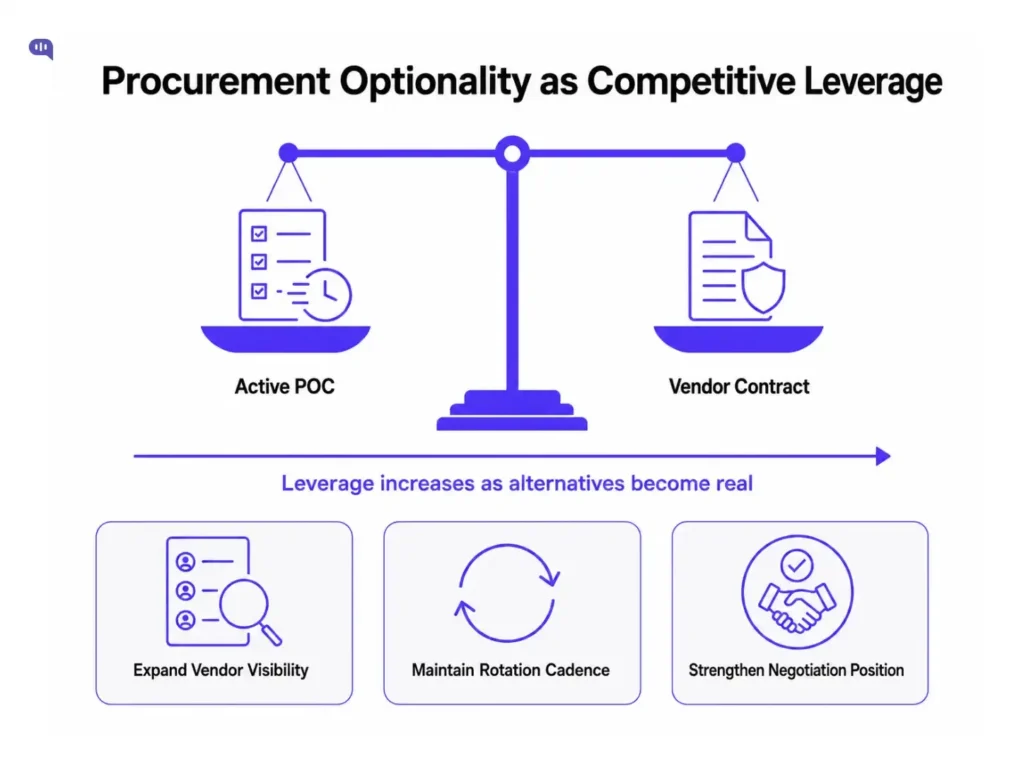

What does vendor diversification actually mean?

The instinct when you hear “diversified vendor stack” is to picture a sprawling multi-tool architecture. But that’s not a practical recommendation.

Diversification at the procurement layer is different from diversification at the deployment layer.

| Layer | Goal | What It Looks Like | What It Is Not |

|---|---|---|---|

| Deployment layer | Focus | One primary platform, deeply integrated with your CRM and knowledge base, runs the majority of the volume | Multiple production systems running in parallel |

| Procurement layer | Optionality | At least one alternative vendor in an active POC; contracts with data portability and exit provisions | A theoretical shortlist that has never been tested |

At the deployment layer, you want to focus. Context fragmentation across parallel production systems creates worse customer experiences, not better ones.

At the procurement layer, you want optionality. That means two things in practice:

- Active POC discipline. At any given time, you should have at least one alternative vendor in a live proof-of-concept environment, running against real or representative support ticket volume. A working integration that a small portion of your team actually touches.

- Contract structure that preserves exit. The vendors most motivated to lock you in are the ones most likely to change pricing or product direction after an acquisition. Standard enterprise SaaS contracts for AI platforms now routinely include multi-year commitments, usage minimums, and data portability terms that are easy to overlook in a favorable market. Reviewing these terms with the assumption that the vendor’s ownership structure may change simply acknowledges current market conditions.

Long multi-year leases only work if your landlord doesn’t change. If you’re subscribing to a deal where the main product is changing, then you need to be prepared. And that preparedness can act as a competitive advantage during times of flux.

How to build a competitive advantage during consolidation?

There is a dimension to this that goes beyond risk management.

Enterprise procurement teams that run systematic POC programs generate real-time competitive intelligence that changes what they can extract from their primary vendor.

A vendor who knows you have a working alternative in the queue behaves differently than one who knows the switching cost would take twelve months and a major engineering engagement. The POC does not need to be production-ready to be commercially useful. It needs to be real enough that your vendor believes you could accelerate it.

This is the natural consequence of a procurement discipline that can improve your leverage during every vendor negotiation.

What enterprises should actually do: A 90-day implementation plan

The consolidation wave in AI customer support is not finished. Every independent AI support vendor that reaches meaningful scale becomes a candidate for the same move that took Cognigy, Forethought, and Fin off the board in under twelve months. Waiting for your vendor to be acquired before building an exit posture is the wrong order of operations.

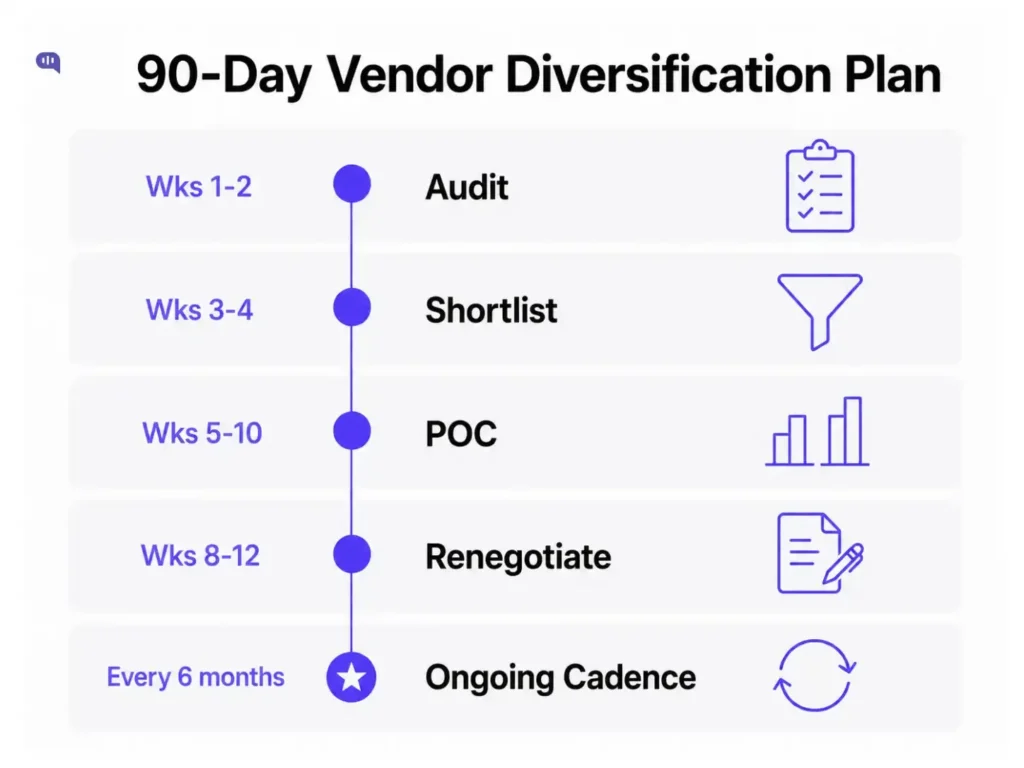

Below is a phased plan for building procurement optionality without disrupting production operations. The timeline assumes a team with at least one dedicated ops or procurement owner and access to your current vendor’s contract.

| Phase | Timeframe | Actions | Owner | Output |

|---|---|---|---|---|

| 1. Audit | Weeks 1-2 | Pull your current contract; flag multi-year lock-in clauses, usage minimums, data portability terms, and notice periods. Map which workflows, integrations, and knowledge sources are vendor-specific vs portable. | Procurement + CX Ops | Lock-in risk register with a clear picture of your actual exit cost today |

| 2. Shortlist | Weeks 3-4 | Identify two alternative platforms that cover your primary use cases. Prioritize vendors with open NLP integrations, MCP-compatible infrastructure, and published data export APIs. Request sandbox access, not a sales demo. | CX Ops + IT | Two shortlisted vendors with sandbox credentials in hand |

| 3. POC | Weeks 5-10 | Run one shortlisted vendor against a narrow, representative slice of your real ticket volume: three to five intent types that make up high volume. Measure resolution rate, escalation accuracy, and integration friction against your current platform baseline. | CX Ops + a small agent subset | Documented performance comparison on a real workload |

| 4. Contract renegotiation | Weeks 8-12 | Use POC results and the existence of a live alternative as leverage at your next vendor touchpoint. Push for data portability guarantees, exit provisions tied to ownership changes, and shorter notice periods. | Procurement + Legal | Improved contract terms or a documented decision to accelerate migration |

| 5. Ongoing cadence | Every 6 months | Rotate the POC to a second alternative. Keep the evaluation muscle active. Treat vendor review as a standing calendar item, not a reactive crisis response. | CX Ops | A continuously warm alternative that prevents leverage decay over time |

A few things worth flagging

- The audit almost always reveals surprises. Most enterprise support teams have never mapped which parts of their AI configuration are truly portable. Conversation flows built inside a vendor’s proprietary builder, knowledge sources indexed in a vendor-specific format, and routing logic embedded in a vendor’s orchestration layer are all switching costs that do not show up in the contract but will appear on your timeline when you try to leave.

- The POC scope discipline matters. Three to five intent types are the right scope for an evaluation POC. Broader than that, and the integration effort exceeds what the POC is worth. Narrower, and you do not generate enough signal to make a meaningful comparison. Focus on your highest-volume, clearest-resolution intents, not edge cases.

- The change-of-control clause is the single most underused contract term in enterprise SaaS. It allows you to exit or renegotiate if the vendor’s ownership changes. Given the current acquisition pace in CX AI, this clause has moved from nice-to-have to essential. Most vendors will push back on it. That pushback is information about how they expect the next eighteen months to go.

How can Kommunicate help?

Kommunicate is built on the premise that enterprise customer support should not require you to choose between capability and control.

Our platform integrates across the major NLP providers, including Dialogflow, Amazon Lex, and IBM Watsonx. It connects to the CRM and helpdesk tools your support team already uses: Salesforce, Zendesk, and Freshdesk. That architecture is intentional. Your support infrastructure should be portable by design, not by exception.

If you are evaluating your current AI vendor posture in light of recent market consolidation, we are a reasonable starting point for comparison. Start a free trial or speak with our team to run Kommunicate against your current environment.

Devashish Mamgain is the CEO & Co-Founder of Kommunicate, with 15+ years of experience in building exceptional AI and chat-based products. He believes the future is human and bot working together and complementing each other.