Updated on June 23, 2026

Key Takeaways

1. The pipeline is leaking. Most carriers respond to declining conversion rates by increasing lead spend. The actual problem is structural: leads are being acquired and lost before meaningful contact is ever made. The insurance lead generation strategy that moves the needle is the one recovering what’s already in the system.

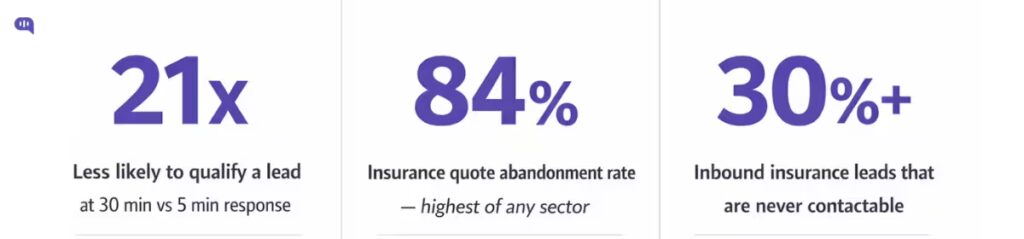

2. The intent window closes in minutes. One of my mentors used to say that once you miss the 30-minute window in contacting your leads, they forget that they filled a form. This was confirmed in a joint MIT and Harvard Business Review study that found that the odds of qualifying a prospect fall 21 times when response time goes from 5 minutes to 30 minutes. Agent-led follow-up cannot operate at that velocity at scale. AI-initiated first contact is the only infrastructure that can.

3. Quote abandonment is the most recoverable revenue problem in insurance. 84% of insurance prospects abandon their quotes. These are high-intent prospects with an unanswered question or unresolved concern. Because acquisition cost is already sunk, AI re-engagement at this stage produces the lowest cost-per-recovered-lead in the entire pipeline.

4. Over 30% of inbound insurance leads are never contactable on the first attempt. LeadSquared’s research across insurance digital marketing teams found that more than 30% of inbound leads go unreached and are simply marked inactive.

5. This is a marketing budget line, not an IT project. Conversational AI for lead recovery sits in the same budget and accountability structure as any other demand generation investment. With 47% of insurance buyers now purchasing through digital channels, the urgency to close the follow-up gap at digital speed is no longer optional.

Why Insurance Pipelines Stall and How Can Conversational AI Recover Lost Leads?

Insurance carriers spend more on digital lead acquisition every year. The budgets are larger, the targeting is sharper, and the volume of inbound quote requests keeps climbing. Yet for most carriers, conversion rates have not kept pace. Quote-to-bind ratios are flat or declining. Pipelines look full on paper and feel empty in practice.

The reflex is to buy more leads.

But lead volume is never the problem.

The majority of leads a carrier acquires never receive a meaningful follow-up conversation. They go dark because the pipeline failed to reach them at the moment they were willing to engage. J.D. Power reports that 47% of all insurance policy buyers now purchase through digital channels, yet the infrastructure for following up with those digital prospects has not kept pace with the volume.

Understanding where pipelines fail, and how conversational AI in insurance recovers what’s already been paid for, is one of the highest-leverage moves available to carrier marketing and distribution leaders right now.

This article will take you through an AI-focused lead retention strategy. We’ll cover:

1. The Pipeline Leakage Problem: What are Insurance Carriers Losing?

2. Top 4 Reasons Insurance Pipelines Stall

3. How Does Conversational AI Solve the Insurance Pipeline Stall Problem?

4. The AI in Insurance Lead Recovery Playbook

5. Where Does AI-led Lead Recovery Fit in on the Org Chart?

6. The KPIs You Should Track for Insurance Lead Generation and Recovery

7. Conclusion

8. Frequently Asked Questions about Insurance Lead Generation

The Pipeline Leakage Problem: What are Insurance Carriers Losing?

The economics of digital lead acquisition in insurance are brutal. Cost-per-lead for personal lines ranges from $15 to over $200, depending on the line of business and channel. At those prices, every lead that exits the pipeline unconverted represents real, quantifiable revenue loss.

Three numbers define the scale of the problem:

There are three core problems here:

1. Speed-to-Contact Decay is Fast and Severe. A joint study from MIT and Harvard Business Review that analysed over 15,000 leads and 100,000 call attempts found that the odds of qualifying a prospect fall 21 times when response time goes from 5 minutes to 30 minutes.

By the time an agent calls back an hour later, the prospect has already compared quotes from competitors, gotten distracted, or simply cooled off. The intent window in digital insurance is measured in minutes, not hours.

2. Quote Abandonment Rates Reach 84% in Insurance. ProPair’s industry analysis finds that insurance carries the highest quote abandonment rate of any sector, significantly above the general e-commerce average of 70%. These are high-intent prospects who demonstrated enough interest to reach the most valuable stage of the funnel, and then fell through.

3. CRM Dormancy is the Industry’s most Overlooked Revenue Problem. LeadSquared’s research across marketing teams in insurancefound that more than 30% of inbound insurance leads are never contactable on the first attempt.

A portion of that pool re-enters the market every quarter, triggered by life events, competitor rate increases, or renewal cycles, with no carrier reaching out.

To put this in perspective, if a carrier’s digital lead CAC is $80 and its first-contact rate is 35%, it is effectively paying $229 for every conversation its agents have.

Every percentage point of contact rate improvement is worth hundreds of thousands of dollars annually at scale.

So, why are contact rates so low for insurance carriers in general? We work with tens of the biggest insurance providers in India and abroad and we have noticed 4 central trends.

Top 4 Reasons Insurance Pipelines Stall

For years, insurance executives follow the same script to handle falling conversion rates. Whenever conversion rates fall, executives blame it on agent performance, asking:

- Are they following up quickly enough?

- Are they using the right script?

- Do they need more training?

But the failure around conversion rates is almost always structural. And even if agent performance can be squeezed for a few basis points of optimisation, the process is expensive and cumbersome.

In our experience, enterprise and mid-market carriers are far more likely to increase conversion rates by focusing on the following four failures.

Failure Mode 1: Speed-to-Contact Collapse

Digital prospects operate in real time. They fill out a quote form expecting an immediate response.

78% of sales go to the first company that responds, but agent-led contact simply cannot operate at the velocity digital intent requires. An agent handling 40 leads a day cannot call each one within five minutes. The infrastructure was never designed to do that.

Failure Mode 2: Follow-Up Inconsistency at Scale

It’s hard to maintain follow-up cadence at scale.

When lead volume is low, agents can maintain a disciplined follow-up cadence manually. As volume grows, the cadence degrades. High-intent leads and low-intent leads receive identical treatment because there is no system prioritising them differently.

A prospect who abandoned a quote at the premium selection screen is treated the same as someone who bounced from the homepage.

Failure Mode 3: Quote Abandonment Silence

A prospect who received a quote and went dark has the highest demonstrated intent in the entire pipeline.

The quoted-not-sold rate is the clearest signal of a recoverable revenue problem. These prospects did not say no. They said not yet, or not sure. Most carrier pipelines have no structured response to this state.

Failure Mode 4: Re-Engagement Timing Blindness

Leads do not die at 30 days. Prospects who went inactive re-enter the market constantly. A carrier that marked a lead inactive six months ago has no mechanism for knowing when that lead becomes relevant again. Without a trigger-based re-engagement system, the carrier is simply absent when the prospect is ready.

None of these failure modes are related to agent capability. Instead, it calls for automations that can help your agents follow up, maintain cadence and engage prospects better. This is something conversational AI can help you solve.

How Does Conversational AI Solve the Insurance Pipeline Stall Problem?

You might have noticed that all the above failure modes are connected to tools that every carrier has. So, the problem lies in how they operate at scale:

- Email drip sequences deliver high open rates and near-zero response loops. A prospect can receive six emails in a sequence, open three of them, and never do anything.

Remember that emails cannot ask questions, respond to hesitation, or adapt to what the prospect actually needs. It is a broadcast, not a conversation. - SMS outreach has the same limitation, compounded by compliance risk. A message that says “Your quote is ready” cannot answer “I saw a lower rate somewhere else” or “I’m not sure I need this level of coverage.” It fires and forgets.

- Agent callbacks are the right intent deployed at the wrong time and scale. The agent is capable of having the exact right conversation, but not within five minutes of every inbound lead, and not at 9 PM, and not for a CRM containing 50,000 dormant contacts.

Conversational AI in insurance fills the gaps that none of these approaches can reach. An AI-powered conversation is two-way and adaptive. It can ask a clarifying question, receive a natural language response, adjust its next message accordingly, and route intelligently to a human when complexity demands it.

It operates at the speed of digital intent, responding within seconds of a quote request, and it scales without constraint. The same system that handles 100 conversations on a Tuesday morning handles 10,000 on the Monday after a major catastrophe announcement without degradation.

This is not a replacement for insurance agents. It is coverage for the moments and volumes where agents cannot physically operate, which, for a carrier running digital acquisition at scale, is a significant portion of the pipeline.

Conversational AI also enhances marketing automation processes. Automation handles scheduling, segmentation, and campaign orchestration & conversational AI handles the actual exchange: the back-and-forth that qualification, recovery, and re-engagement require.

These benefits from conversational AI scale a lot better when you have playbooks that operate alongside your ongoing marketing and sales efforts. We’ve compiled a few strategies that can help.

The AI in Insurance Lead Recovery Playbook

Lead recovery is very nuanced.

Different pipeline stages have different failure dynamics and respond to different conversation strategies. Here is where AI intervention produces the clearest return:

Stage 1 – Immediate Follow-Up: The First 5-Minute Window

This is the highest-ROI deployment of conversational AI in a carrier’s pipeline. You can connect your intake form with an AI chatbot that initiates a conversation whenever a lead is generated. The conversation confirms intent, captures missing information, handles the most common early questions, and either qualifies the lead for immediate agent handoff or schedules a callback at the prospect’s preferred time.

The effect on contact rate is consistent across deployments: response rates from AI-initiated first contact are significantly higher than agent-initiated callbacks that occur an hour or more after inquiry. The prospect is still in the intent window. The carrier is still the first voice they heard.

Stage 2 – Quote Abandonment Recovery: Your Highest-Intent Lost Leads

A prospect who received a quote and went quiet is not a lost lead. They are a prospect with an unanswered question, an unresolved concern, or a timing issue, all of which a conversation can surface and address.

Marketing automation initiated at 24 hours, 72 hours, and seven days after quote delivery consistently recovers a meaningful portion of abandoned quotes. The first message might probe for a price concern. The second might ask about coverage questions. The third might simply ask if now is still a good time.

And when the prospect replies with their concerns, conversational AI can take over, answer FAQs and help them through the binding process.

Because the CAC for these leads is already sunk, the cost-per-recovered-lead in this stage is extremely low. Even a 5% recovery rate on abandoned quotes at a carrier processing 10,000 quotes per month represents 500 additional conversations. This volume of conversations can’t be replicated without hiring a lot of insurance agents.

Stage 3 – Dormant Lead Reactivation: The 30/60/90-Day Recovery Window

The carrier’s CRM is its most underused revenue asset. Dormant leads are not dead leads, they are prospects whose timing did not align with the carrier’s follow-up window. Life circumstances change. Rates from competitors increase. Renewals approach.

Your marketing team is probably already running reactivation sequences triggered by external signals (renewal season, major weather events that prompt home insurance reviews, competitor rate announcements) or run on structured timing intervals.

The change here is having AI there for instant query resolution whenever a prospect replies to these reengagement messages. For example, if a prospect is clicking on a retargeting ad on Instagram, it’s important to have an AI agent that can reply and pre-qualify them on the same channel.

The critical metric here is cost-per-recovered-lead measured against new lead CAC. If the carrier’s new lead CAC is $80 and the retargeting sequence with AI agents recovers 2% of a 50,000-lead dormant pool at an automation cost of $1.50 per contact, the math is decisive.

Across these stages, AI agents play second fiddle to your pre-existing marketing automation workflows. Since insurance agents have limited time to engage with every prospect, it makes sense to drive the engagement with conversational AI and then transfer it to the right agent. And given that carriers already run these retargeting and reengagement campaigns at scale, the playbook can drive meaningful revenue without impacting overall budgets.

Where Does AI-led Lead Recovery Fit in on the Org Chart?

Since AI is nascent and hasn’t been deployed at a large scale across the insurance industry, the question around ownership is often met with silence. The technological base is solid, there are proven use cases and pilots, but without proper ownership, AI-led lead recovery ends up in a dusty file cabinet.

However, this is not a complicated question to begin with. Lead recovery sits within the marketing budget, and conversational AI for insurance teams should complement existing lead recovery efforts when deployed.

Most enterprise organisations that work with us follow a similar cadence

| Function | Responsible (R) | Accountable (A) | Consulted (C) | Informed (I) |

| Marketing / Distribution | Campaign execution, messaging, conversation playbooks, & lead journeys | Owns growth outcomes and pipeline impact | Compliance (for messaging approval), Contact Centre (handoff quality) | IT, Finance |

| IT / Technology | Integrations (CRM, APIs), infrastructure, data pipelines, & security implementation | Owns system reliability, data integrity, and scalability | Compliance (security/legal), Marketing (tooling needs) | Contact Centre, Finance |

| Contact Centre / Agents | Handling AI handoffs, disposition tagging, & feedback loops on conversations | Owns resolution quality and customer experience outcomes | Marketing (intent design), IT (tool usability) | Finance, Compliance |

| Finance | ROI modelling, cost tracking, & budget monitoring | Owns financial guardrails and program viability | Marketing (growth assumptions), IT (cost structure) | Contact Centre, Compliance |

| Compliance / Legal | Regulatory approvals, audit trails, policy enforcement | Owns regulatory risk and legal exposure | IT (data handling), Marketing (scripts and outreach) | Finance, Contact Centre |

While actioning this, you should note two things:

- The IT integration scope for a conversational AI lead recovery deployment is typically a one-week project, and not a full transition. Framing it as the latter is how it ends up in a twelve-month backlog.

- The conversation playbooks are marketing assets, written and owned by the marketing team using the same voice guidelines as any other customer communication. They do not require engineering resources to maintain or update.

With proper ownership, the change management question for agents is also resolved quickly.

AI handling first contact and dormant re-engagement means agents spend more time on warm, qualified conversations and less on cold callbacks that go to voicemail. That is an improvement to the agent workflow.

Carriers that communicate this clearly during rollout see significantly less internal friction than those that do not. Ultimately, the cleaner the ownership is at the start, the faster the deployment moves and the sooner the KPIs are being measured.

And on the subject of KPIs, there are a few recommended KPIs to track to maintain lead re-engagement quality.

The KPIs You Should Track for Insurance Lead Generation and Recovery

Building the internal business case for AI-based lead recovery requires a small, defensible set of metrics. Here are the four that matter:

| KPI | What it measures | Benchmark |

| Contact rate lift | % of leads reaching a meaningful two-way exchange before and after AI deployment | 40–80% improvement vs baseline |

| Quote-to-bind delta | Conversion rate change on AI-re-engaged leads vs non-re-engaged leads | Measurable lift within 90 days |

| Cost per recovered lead | Total AI programme cost ÷ dormant or abandoned leads that returned and converted | Compare directly against the new lead CAC |

| Pipeline velocity | Average days from lead→quote and quote→bind — does AI compress either window? | Maps to revenue cycle efficiency |

A carrier that tracks these four metrics quarterly has everything it needs to demonstrate ROI, make the expansion case, and identify which pipeline stages are delivering the strongest return.

Just for context, a recent enterprise carrier we onboarded has reported that their quote-to-bind rates increased by 40% for a recent client who used Kommunicate chatbots to drive first contact on their website.

Conclusion

The most important shift in how carriers think about lead generation is also the simplest: the pipeline is not empty. It is leaking.

For most carriers, the leads needed to hit this quarter’s growth targets already exist: in the quote abandonment log, in the dormant CRM segment, in the inbound requests that went unanswered past the five-minute window last week.

Conversational AI in insurance does not change where leads come from. It changes what happens to them after they arrive. That is a fundamentally different value proposition from buying more traffic or hiring more agents. It is a recovery argument, not an acquisition argument, and for marketing directors accountable for both topline growth and cost efficiency, it is often the faster path to both.

If you want to set up an insurance lead recovery system for your org, feel free to book a demo with Kommunicate.

Frequently Asked Questions about Insurance Lead Generation

Insurance lead generation is the process of identifying and attracting prospective policyholders. At the agent level, this typically means sourcing names to call. At the carrier level, it means building and funding the digital channels that produce inbound quote requests at scale.

The distinction matters because carrier-scale lead generation is an infrastructure and conversion problem, not a prospecting problem. Most carriers are not underinvesting in lead acquisition. They are underinvesting in what happens to leads once they arrive.

Carriers generate leads primarily through paid digital channels. The challenge is not generating volume. At scale, the conversion bottleneck is almost always speed-to-contact and follow-up consistency, not channel performance.

An insurance lead generation strategy that focuses exclusively on acquisition while leaving follow-up infrastructure manual will consistently underperform one that invests equally in recovery and re-engagement.

Lead generation is acquiring new prospects. Lead recovery is converting prospects you have already acquired but failed to reach or convert on the first attempt. Most carriers treat these as the same problem and respond to declining conversion rates by buying more leads.

They are separate problems requiring separate infrastructure. Lead recovery typically produces a lower cost-per-conversion than new lead acquisition because the marketing spend is already sunk. For most carriers running digital acquisition at scale, the lead recovery opportunity is larger than the new acquisition opportunity.

A standard insurance chatbot operates on predefined scripts and decision trees. It can answer a fixed set of questions, and when the prospect says something unexpected, it fails or escalates. Conversational AI uses natural language processing to understand intent, maintain context across a conversation, ask follow-up questions based on responses, and adapt its path in real time.

In a lead recovery context, the difference is significant: a chatbot can confirm a quote is ready, but conversational AI can ask why the prospect hasn’t bound yet, handle a price objection, answer a coverage question, and route to the right agent with context attached. The latter is what closes the pipeline gap. The former is what creates the illusion of follow-up without the substance.

The primary regulatory frameworks that apply are TCPA (Telephone Consumer Protection Act) for SMS and voice outreach, and state-level insurance communication regulations that govern what can be said to prospects before a policy is in force. AI-driven outreach is not exempt from either.

Conversation scripts need compliance sign-off before deployment, particularly for any outreach touching Medicare or health insurance lines where CMS rules apply. The practical implication for deployment: compliance is a consulted function at the design stage, not a reviewer at the end. Building conversation playbooks with compliance input from the start is significantly faster than retrofitting scripts after the fact. This is one reason the deployment timeline for conversational AI lead recovery is measured in weeks rather than months when ownership is clear.

Contact rate improvement is typically visible within the first two to four weeks of deployment, because it is a direct function of response time, which changes immediately when AI initiates first contact.

Quote-to-bind delta and cost-per-recovered-lead take longer to measure reliably, because they require enough volume moving through the re-engagement sequences to produce statistically meaningful conversion data. A carrier processing meaningful digital lead volume should expect to have a defensible read on all four core KPIs within 90 days. That is the right timeframe to set expectations with leadership when making the internal business case.

The mechanics work across both, but the conversation design differs significantly. Personal lines lead recovery involves high volumes of relatively standardised leads where speed and consistency are the primary variables. Commercial lines involve longer consideration cycles, multiple decision-makers, and more complex coverage questions.

Conversational AI in commercial insurance is better deployed at the qualification and re-engagement stages than at immediate first contact, where the prospect’s needs typically require more nuanced discovery before a conversation adds value. The same platform can serve both, but the playbooks, timing, and handoff thresholds should be built separately.

The core integration requirement is connecting the conversational AI platform to the carrier’s CRM.

For most carriers running standard CRM infrastructure (Salesforce, HubSpot, or an insurance-specific system), this is an API integration that takes one to two weeks. Policy administration system integration is optional at launch and typically added once the lead recovery playbooks are proven. The conversation playbooks themselves are built and maintained by the marketing team, not engineering.

The IT scope is narrower than most stakeholders assume, which is why framing this as an IT project rather than a marketing initiative is the most common reason deployments stall before they start.

Devashish Mamgain is the CEO & Co-Founder of Kommunicate, with 15+ years of experience in building exceptional AI and chat-based products. He believes the future is human and bot working together and complementing each other.